Jungheinrich | Value Hiding In Plain Sight

Intralogistics - A Rapidly Growing TAM And Second Level Beneficiary of E-Commerce

Company: Jungheinrich Aktiengesellschaft

HQ: Hamburg, Germany

Ticker: (Frankfurt: JUN3)

Market Cap: €2.89 Billion Euro (share price €28.35)

Public Float: 47% Preferred shares

URL: https://www.jungheinrich.com/en

Strategy: Undervalued, buying opportunity

Who are Jungheinrich? And what is Intralogistics?

Jungheinrich is a business that is 53% family owned but with public shareholders accounting for the other 47%.

It was founded by Dr. Friedrich Jungheinrich in Hamburg in 1953 and operates in Intralogistics.

In terms of the movement of physical goods, the pressure to perform has never been greater. Automation in warehouses has become critical in order to meet demanding service level agreements, to manage exponential SKU growth, to satisfy rising customer expectations, and to address labour challenges.

Intralogistics involves the introduction of systems to address all of these challenges.

Companies such as Amazon have set the bar at a high level and others need to learn how to jump in order to remain competitive.

Unlike Amazon which manages its own intralogistics, Jungheinrich supplies intralogistics solutions to other companies - its customers.

Jungheinrich Aktiengesellschaft, through its subsidiaries, provides equipment, automated systems, digital solutions, and matching services. It also has a financial services arm that is concerned with sales financing and leasing.

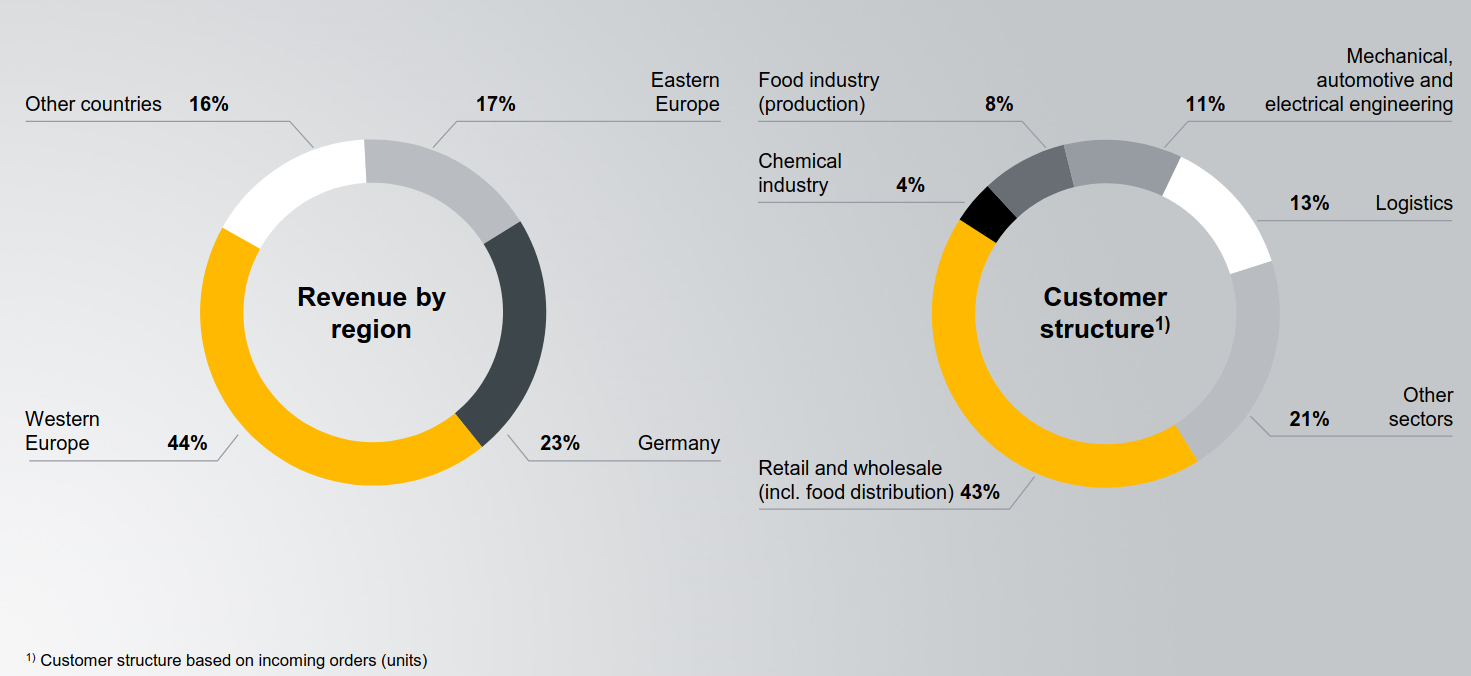

In 2022, its more than 19,000 employees helped it to achieve global revenue of €4.2 billion Euro. Its products and associated services are marketed via direct sales, plus it has an extensive distribution network in Europe, Asia, Africa, Australia and South America.

The business enjoyed an IPO back in 1990, the same year as the German reunification after the Berlin wall had fallen. The business responded to the pent-up demand for modern industrial trucks and warehouse equipment in the new German states and the former Eastern Bloc countries. This was a major catalyst for growth.

Then came the era of globalization and the company went from strength to strength.

Customer-first orientation, technical leadership and outstanding service are deep-rooted in the history of the company.

When you think of Jungheinrich today you think of reliable products, sophisticated solutions and innovation with real added value. It represents a reliable, one-stop shop for everything from planning and analysis to digital controls; from racking and warehouse equipment to sophisticated energy options and a global service network. Everything it does is focused on optimizing the process flows of its customers, raising warehouse productivity and lowering operating costs.

Today Jungheinrich counts among the top three intralogistics brands worldwide.

It has a very strong brand built on the solid foundation of its family values. This aligns the interests of the management with that of long term shareholders. It states in its corporate literature, and on its website, that long-term business relationships are far more important to it than short-term deals and this is wonderful to hear. The best investments are those run by people with a long term perspective.

This is critical. Think Warren Buffett, Jeff Bezos, Sam Walton, Henry Singleton and so on, all of whom operated on time horizons measured in decades.

Management must be concerned with creating an enduring enterprise. It needs to be focused on customers and on its employees, on its input costs and its revenues. It should be entirely unconcerned about the day-to-day fluctuations in its share price.

This latter part may seem odd to most investors but it is so critically important. A successful company is one that can grow organically without needing to raise additional money via capital markets. Ergo, if it intends not to issue any more shares, the share price doesn’t matter.

Focus on building the business and the share price will eventually look after itself.

All of that to say, Jungheinrich is the right kind of company with the right kind of management for an intelligent investor. It’s all about long term thinking.

In addition to organic growth, it also seeks out accretive acquisitions. Recently it acquired Munich-based autonomous mobile robot (AMR) developer Arculus GmbH. In so doing it enlarged its robotics and software portfolio which it will use to help customers design the warehouses of the future. This is higher margin business and so that bodes very well for the future of the business.

It also acquired Storage Solutions, a leading provider of ready to use racking systems and warehouse automation in the USA. This is important because to date Jungheinrich has had little or not exposure to the US market. This acquisition will assist in growing that market segment. It provides more geographic diversification.

2022 was the best financial year to date in the history of Jungheinrich and this year looks even better, yet the business is currently being valued where it was back in 2017 when revenues were 30% lower, economic earnings were 45% lower and economic earning margins were nearly 300 basis points lower (9.8% vs 12.5% on an LTM basis).

The company has a solid balance sheet with cash and short term investments of over €500 million plus credit facilities of €305 million with very low utilization. It has an investment grade credit rating, testament to its stability, with the added benefit that it has access to lower cost financing.

Its equity ratio is increasing steadily from €1.36 billion (29% of assets) back in 2018 to €2.05 billion (33% of assets) by 2022.

Guidance

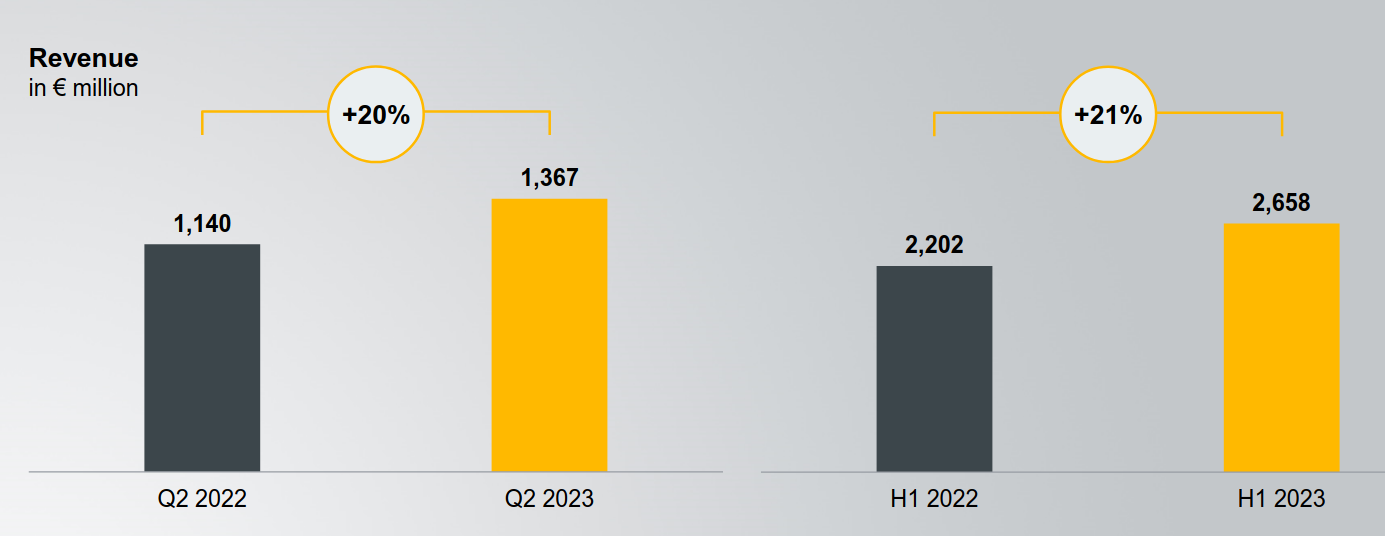

Revenues are growing strongly, and this is partly fueled by the new acquisitions.

Operating leverage results in stronger growth in operating earnings on an EBIT basis. Most encouraging is that margins are expanding. The company use Return on Sales, but this is effectively Operating Margin calculated on an EBIT basis. These have expanded by 110 basis point on a quarterly YoY basis and 150 basis points on a semi-annual YoY basis.

The company has a 2025 strategy which it is well on target to meet. Full time R&D workforce has increased from 810 to 980 (+21%) while total full time employees grew from 19,807 at the end of 2022 to 20,445 six months later (+6% annualized). This is a strong indicator about the confidence of the management and the direction of travel.

Free cash flow has been negative due to the heavy CAPEX investment in growth. This will soon start to pay dividends. Without the growth CAPEX, free cash flow would have been €182 million for H1 2023 (€364m annualized), implying a free cash flow yield of 12.55%.

Return on Capital Employed has increased from 14.4% to 18.2% on an annualized basis.The company's guidance is based on the assumption that the global economy will continue to grow in 2023, albeit at a slower pace than in 2022. Jungheinrich also expects the supply chain disruptions that have plagued the industry in recent months to ease in the second half of the year.

The global demand for intralogistics solutions is expected to grow in the coming years, as businesses invest in automation and digitization to improve efficiency and productivity. This is largely, but not exclusively, fueled by growth of the e-commerce market in which retailers need to invest in automated warehouses and fulfillment centers to handle the growing volume of online orders. All of this bodes will for Jungheinrich.

Jungheinrich is expanding into new markets, planning to make its mark in the US following its recent acquisition and also moving into Asia and South America. This expansion ought to drive growth in the coming years.

Financials

Top line is growing steadily year on year (5yr CAGR 7.8%) and, more particularly, with an operating leverage multiplier of approximately 1.5x, this ought to push adjusted economic earnings growth of closer to 12%.

The management run the business very tightly. Gross profit margins are consistently around 30% and OPEX remains in a tight range of 45% to 50% of gross profit.

Long term leverage is held steadily at around 3x, asset turnover 0.8x and margins have expanded and are likely to expand further.

The company currently has 102m shares outstanding, a number that has remained unchanged since 2005. The company is perfectly able to support itself without resorting to issuance of new equity and, more importantly, the company does not engage in any form of stock based compensation. Accordingly, there is no dilution for shareholders to be concerned about.

Competitors

Kion Group AG (another German company with strong brands such as Dematic, STILL, Linde and Baoli) is probably the largest listed competitor in the intralogistics industry. Having already established itself in Europe and the Americas, Kion has set its sites on a new growth path: China. It is currently expanding its sales and service network through distributor partnerships, the most recent of which is in Xi’an, the capital of Shaanxi Province. It is looking to capitalize on China’s growing demand for intralogistics solutions and is definitely well positioned to do so.

My analysis would suggest that Jungheinrich is not only the superior business with better returns on invested capital, but is is also trading at a significant discount to fair value which creates a margin of safety for an investor today.

Most other competitors are privately owned and include Arvato, a division of Bertelsmann; Boston Dynamics, now owned by Hyundai Motor Group; and Gideon Brothers which recently received investment from DB Schenker.

ESG Credentials

Not only is the business focused on economics, but also on wider social values. It has converted all of its sites in Germany to exclusively run on green energy, this includes six major production plants. The long-term goal is to eventually convert all of its foreign sites to green energy and to produce its own solar power by equipping photovoltaic systems to their sites.

In 2022, Jungheinrich was ranked second in the world for material handling equipment sales by the International Material Handling Federation.

In 2021, Jungheinrich was named the "Most Sustainable Intralogistics Company" by the German Sustainability Award.

In 2020, Jungheinrich was awarded the "Top Employer" seal for its employee-friendly working conditions.

Caveats

Of the total number of Jungheinrich AG shares (102 million), the public float is 47% (48 million no-par-value preferred shares). The 54 million ordinary shares that are not listed are held equally by the families of the two daughters of founder Dr Friedrich Jungheinrich. The preferred shares require the payment of a regular dividend which is anathema to me because there are far better uses for corporate capital.

The shares appear to me to be trading at less than 50 cents on the Euro, in other words well under their intrinsic value, but the very conservative management has a playbook from which they are not prepared to deviate and so share repurchases are off the menu. This is a shame because at the current time this would be the most accretive means of allocating capital.

I challenged the management on this point. The excuses were disappointing. They said:

Preference shares are assured a dividend. While this is certainly true, it could be changed with shareholder consent and how many shareholders wouldn’t consent to larger total returns?

The float is relatively small and that if they were to repurchase stock it could only be the public stock repurchased which would reduce the free float and take the company closer and closer to private ownership which they do not want. However, 47% doesn’t seem that small to me and they would only repurchase stock to the point that market value reached equilibrium with intrinsic value, so the repurchase operation would cease long before the free-float was exhausted. Additionally, they could very easily repurchase both public and private shares so that the ratio of ownership remains unchanged. They ought to take a leaf out of the Henry Singleton playbook. He repurchased 90% of the shares outstanding at Teledyne and not a single shareholder complained about the riches he bestowed on them.

The company is majority owned by the family and it needs to run in accordance with the wishes of the family. My view is that my repurchase proposal would be financially beneficial to the family, so perhaps someone should take the time to explain it to them. Reading between the lines, I imagine that the family holding is in trust and that capital appreciation is not a focus because the beneficiaries are not permitted to draw down capital. If this is the case then the only thing that matters to the family is income (dividends). If I am correct then the family don’t care about the share price and this means that there is a conflict between what the family desires and what would be best for external shareholders.

So, while the company is great and available at a great price, there is an issue here to bear in mind as an external investor. Perhaps this is why the stock trades at a discount to fair value. Said differently, the stock may not reach its fair valuation anytime soon (or ever), although the share price did trade in the mid €40s from April 2021 to January 2022, which is 60% higher than where it stands today – and the unit economics are better today than they were back then, so a revaluation is likely at some point.

Valuation

First, let’s look at what has driven shareholder returns over the past half a decade. Since 2017, revenue has grown from €3.4 billion to €5.2 billion (CAGR 8.77%). This has been the biggest driver of returns, augmented by margin expansion – my economic earnings margin increased from 10.0% to 12.8% (CAGR 4.99%). The share count has remained unchanged so there has been neither a dilution nor a concentration of returns, but there has been an average dividend of 1.71% over the period. All of these are catalysts for positive shareholder returns, but have been cancelled out by an unjustifiable multiple contraction. The company was capitalized at 11.7x economic earnings in 2017 but today, inexplicably, this has contracted to 4.29x. This contraction has resulted in the share price trading down from €39.35 to €28.35. The upshot is a negative shareholder return of 21.1% over the five years.

This is a trade set up that I like to see. The unjustifiable losses of yesterday’s investors will unwind to magnify the returns of investors today. My assumptions are that with recent acquisitions and global expansion, top line continues to grow at 8% CAGR (relatively conservative). That the share count remains unchanged. That economic earnings margin expands only slightly from 12.77% to 13.00% (which is also conservative given that the business will benefit both from economies of scale and also expansion of higher margin digital service segments). That the dividend continues at 1.71%. Finally, that the business will see a multiple expansion to a more reasonable 10x economic earnings (super conservative as that implies that it will be capitalized at 1.3x sales on a 13% economic earnings margin and a 10% investor earnings yield). This will be a catalyst for an annual boost of over 19% in shareholder returns. If the company achieves this in the next five years, then the shares are worth 3x where they trade today. Share price appreciation plus dividends will result in 268.4% total return (29.8% CAGR). Even if it only achieves half of this, the returns would still be very good, so that is a considerable margin of safety.

Conclusion

I always look for signs of competent management who are thinking like owners and that appears to be the case with Jungheinrich.

The average tenure of the management team is 8.8 years. The CEO has been in the business for just under nine years himself and the CFO is in his fourteenth year in the business. So these are not career executives focused on short term bonus targets with one-eye on the next job.

For a company to be valuable it must grow and endure, but many CEOs focus only on the growth part and then only on a short-term basis. Jungheinrich has long term management with a long term focus. They are interested in doing what is best of the majority family owners and that, for the most part, aligns with what is best for external shareholders also (except for their capital allocation policy which favours dividends to the exclusion of better alternatives).

The business appears to be run like a military operation with German efficiency. Everything from the margins that the business generates to its cash and debt levels and its discipline around both OPEX and CAPEX spending is remarkably stable over the long term (more than a decade). This is encouraging and the predictability mitigates downside risk, particularly given the unjustifiable draw-down in the stock recently.

This appears to be a buying opportunity with an asymmetric skew to the upside that favours an investor.

Disclaimer:

Views, information and opinions expressed in this analysis are those of the author. They should neither be construed as investment advice nor as a recommendation to buy or sell any particular security. Security specific information should not be relied upon as the basis for your own investment decisions. You must do your own research, seek independent advice and reach your own conclusions.

The author may have a position in securities named in this article and may change those position at any time

How are you calculating economic earnings? thanks