Melrose Industries | A Pivotal Moment

A very interesting aerospace engineering opportunity

Disclaimer & Disclosure: The author has a long position in Melrose. This post is for informational purposes only and should not be construed as investment advice. Conduct your own due diligence and seek professional investment advice before making any investment decisions.

Melrose Industries Plc (London: MRO.L)

Market Cap GBP £6.6 billion

EV GBP £7.7 billion

Float 94.3%

NTM EV/Revenue 2.1x (against 2025 operating margin ~18%)

Important Readers’ Notes (please read)

This investment opportunity requires a detailed understanding of the recent developments and future potential of the business. The company has undergone a monumental pivot, rendering historical data largely irrelevant. The focus needs to be on grasping the intricacies and nuances of the new business structure. This pitch needs to be properly understood, so please read this analysis carefully and thoroughly.

A Financial Times article by Bryce Elder, published on August 23, 2024, discusses Melrose Industries, but in my humble opinion it completely misrepresents the business. The article heavily relies on a Union Bank of Switzerland (UBS) report that downgraded Melrose's stock rating from "buy" to "sell", yet the UBS report contains significant flaws in its analysis.

This analysis will break down why Melrose's financial outlook is far more favorable than UBS's assessment.

Melrose is legally entitled to a multi-decade, high-margin revenue stream, which the company estimates has a net present value of approximately GBP £5.7 billion (against a current market cap of GBP £6.5 billion), yet UBS's modeling arrived at a significantly lower figure of £2.8bn.

UBS seemed to misunderstand the nature of the business and particularly the benefits that flow to Melrose by virtue of its RRSP contractual agreements (explained below). Cash lags profit in this business because accrual accounting practices require that when the engine is shipped, some of the contractual revenue and profit that will flow under the RRSP needs to be booked to the income statement, yet the cash arrives and appears in the cash flow statement sometime later. It is also worthy of note that UBS used some questionable numbers in their models, such as a discount rate of 9% compared to the 7.5% used by Melrose. UBS seemed to be quibbling over accounting conventions, meaning that they were so deep in the weeds of quantitative analysis that they entirely missed the qualitative aspects of this phenomenal business.

If UBS did misunderstand the Melrose business and its potential, then the Financial Times made matters a whole lot worse when it presented the UBS conclusions without independently verifying them. The article’s publication by such a reputable news source gave undue credibility to a flawed report and made it available to a far larger audience.

The UBS analysis set a share price target of 400 pence, significantly below Melrose's trading value at the time, and this was included in the Financial Times article. Needless to say, the market reacted to this widely disseminated report, adopting a herd mentality which caused a substantial decline in the share price.

This discounted share prices becomes a key element of this thesis, because what was already a great business, is now a far more attractive investment opportunity based on its low valuation (perhaps we should thank UBS after all!)

This report aims to clarify the facts, enabling readers to make an informed assessment of Melrose's investment potential.

Looking at the Melrose Industries share price chart above, the eagle-eyed reader will spot a huge spike in 2016. This was triggered by the sale of its subsidiary, Elster, a gas and electricity metering business, to Honeywell International for GBP £3.3 billion. At that time, Melrose's raison d'être was to acquire, improve, and sell businesses. The Elster sale yielded a high return on invested capital, prompting the company to return GBP £2.4 billion of the proceeds to shareholders through a share buyback program, resulting in the repurchase of over 80% of its shares outstanding. This move sharply increased the price of the residual shares.

While not directly relevant to this analysis, it demonstrates how committed Melrose has always been to maximizing shareholder value, and this ethos continues today.

Overview and History

Melrose Industries (London: MRO), founded in 2004, operated with a straightforward strategy for many years: acquire, enhance, and eventually sell underperforming industrial businesses. This approach proved successful for over a decade. However, in 2018, the company underwent a major transformation with its acquisition of GKN (formerly Guest, Keen & Nettlefolds), an historic British engineering firm established in 1759.

For history enthusiasts, GKN's legacy spans over 260 years, playing a significant role in Britain's industrial growth. The company originated from the Dowlais Ironworks, which produced cannonballs for the British army during the Napoleonic Wars, including those used at the Battle of Waterloo in 1815. Throughout its history, GKN evolved into a major iron, steel, and coal conglomerate, entering the automotive sector in the early 20th century. It became a prominent automotive parts manufacturer and contributed to both World Wars, supplying steel for military use and producing Spitfire components during World War II. The acquisition of Westland Aircraft's helicopter manufacturing business in 1994 marked GKN's formal entry into aerospace.

Fast forward to modern times and GKN had become a multifaceted entity with operations spanning aerospace, metallurgy, automotive, and ironworks. However, as is the case with every great company, sooner or later it will come under the control of poor leadership. It faced significant financial and operational challenges in the years leading up to 2018, including profit warnings, a substantial pension deficit, and general concerns about the management team. These issues culminated in a loss of investor confidence and made the company vulnerable to takeover attempts.

Melrose identified this opportunity and launched a hostile bid, raising its offer to £8.1 billion after initial resistance from GKN's board, and this is how Melrose acquired GKN.

The takeover was controversial due to concerns about the impact on GKN's pension scheme, long-term strategy, and potential national security implications as GKN was a major supplier to the U.K. defense industry.

Melrose arguably overpaid for GKN, which became evident when the company had to write down some of its balance sheet goodwill linked to the carrying value of the powder metallurgy division - this could have been due to Melrose having inherited GBP £629 million worth of lossmaking contracts when the deal was struck. Then the COVID19 pandemic in 2020 created unforeseen challenges, including automotive supply chain disruptions due to a semiconductor shortage and the grounding of civil aviation fleets amid lockdowns and travel bans.

Melrose, known for optimizing cash flow from acquired businesses through stringent inventory management, found these measures insufficient during the pandemic, making divestment necessary. It took the decision to spin-off the GKN Automotive and Powder Metallurgy businesses in 2023. These were listed as Dowlais Group on the London Stock Exchange, paying homage to the original Dowlais Ironworks.

Melrose faced public criticism for dismantling an historic British institution, but the company needed to streamline GKN's operations.

Emerging from this process, Melrose became a leaner company, retaining GKN Aerospace, which it viewed as the "jewel in the crown." This business revealed itself to be something of a long-term cash-cow, as shall be explained below. So Melrose capitalized on the opportunity to transform itself from an industrial turnaround vehicle, into a singularly focused aerospace business, which is what it is today.

This shift forms a key part of the investment thesis. It is rare for a company with a successful track record of generating substantial returns through short- to medium-term industrial turnarounds to pivot to a long-term, single-business focus. This suggests that Melrose believes GKN Aerospace represents an exceptional opportunity.

Today, it appears that we have the opportunity to invest in that truly exceptional business at a discounted market price.

Significance of the Recent Pivot

The Melrose Aerospace business comprises two primary divisions: Structures and Engines.

The Engines division focuses on engine components and systems, including risk and revenue sharing partnerships with major manufacturers, and is expected to contribute over 70% of Melrose's profit by 2025, primarily from a strong aftermarket business targeting a 28% operating margin. In contrast, the Structures division specializes in aerostructures and high-voltage electrical systems but is currently less profitable and undergoing restructuring to improve margins, aiming for 9% by 2025. While both divisions serve civil and defense aerospace markets, the Engines division is the primary driver of growth and profitability for Melrose.

Melrose finds itself with a very favourable position in the value chain in respect of both.

Improvements in the fundamentals of the Engine segment are impressive when graphically represented:

A key aspect of Melrose’s business is the value derived from Risk and Revenue-Sharing Partnerships (RRSPs). These long-term agreements with major engine manufacturers - such as Pratt & Whitney and GE in the U.S., Safran in France, and Rolls-Royce in the U.K. - allow Melrose to earn income from initial production as well as from long-term, higher-margin maintenance fees.

Risk and Revenue-Sharing Partnerships (RRSPs) are a foundational contractual model in the aerospace industry, yet poorly understood by investors.

When a new aircraft is developed, the design is typically centered around the latest engine technology. Engine manufacturers supply engines at slim profit margins to aircraft manufacturers - a de facto duopoly of Airbus and Boeing, both of which have plenty of pricing power.

However, once the aircraft are sold to airlines, they’re not just handed over with a handshake and a set of keys. They come bundled with long-term service agreements that cover the aircraft’s entire operational life. This is where the real money is made. While engine sales may be low-margin, the ongoing maintenance, repair, and overhaul work - known in the industry as the "aftermarket" - is much more lucrative. This work continues for decades, and the bulk of the returns for companies involved in RRSPs come from this phase, not the initial sale.

At first glance, it might seem like airlines are getting the short end of the stick - buying expensive aircraft and signing up for pricey service deals. But that’s not quite right. It’s better to think of these service agreements as a form of insurance. They’re tied directly to engine usage, so as an aircraft racks up flight hours, the payments increase. Many agreements follow a "power-by-the-hour" model, where airlines pay for maintenance based on how many hours the engines are actually flown.

This setup creates a strong alignment of interests. The companies in the RRSP benefit when the aircraft stay in the air, because that’s when revenue flows in. Airlines also benefit from keeping their planes flying as much as possible - they’ve invested heavily in the fleet and want maximum return. In this way, both sides are incentivized to ensure that aircraft remain in service for as long and as often as possible.

A commercial jet engine is built to last for decades and it is estimated that a typical commercial jet, such as a Boeing 737 or an Airbus A320, can accumulate an incredible 20 to 30 million miles over its useful life. But here's something to think about: over those years, almost every part of the engine will be replaced at least once. So, is it still the same engine by the end of its life? That’s the classic Theseus Paradox in action.

It’s an interesting philosophical question, but from an economic standpoint, it doesn't really matter. The value lies in keeping the engine operational, regardless of how many parts are swapped out along the way. So while it may not be the original engine in a literal sense, it still plays the same role—and keeps generating revenue mile after mile.

Regardless of which engine manufacturer is involved, the engine's components are outsourced to a network of specialized aerospace engineering firms like Melrose (GKN). For example, a Rolls-Royce engine is assembled with contributions from multiple specialist firms, making it a collaborative, syndicated effort. This is all documented in the RRSP. These agreements define how each member of the syndicate shares both the risks and revenues over the contract’s duration.

Under an RRSP, Melrose might receive, for example, a 5% share of both the risk and revenue flowing from deployment of the engine. What makes the RRSP structure particularly advantageous is that for every dollar of revenue generated over the engine’s lifetime, each syndicate member receives its share, regardless of whether it performed any maintenance work.

This is a huge benefit to Melrose in particular, because it focuses on producing structural components of the engine, such as non-moving parts that house the engine and attach it to the aircraft. These include hardware like engine mounts and turbine cases, which are critical but do not rotate and thus are less prone to wear and tear. By specializing in these parts rather than high-stress, rotating components, Melrose minimizes its ongoing operating expenses related to maintenance obligations. While the other syndicate members are doing the heavy lifting in respect of service and maintenance work, Melrose still receives its share of all maintenance fees paid by airlines.

This approach not only results in high margins for Melrose but also enhances the predictability of Melrose's long-term cash flows. As a result, its revenue streams and earnings are highly robust and durable over the long term.

“Our work is largely complete when the engine is built, while we are entitled to lifetime share of the aftermarket profits. Our RRSPs will deliver an estimated £22bn of lifetime net cash inflow (£5.7bn NPV) for the business. “

Peter Dilnot, CEO, Melrose Industries

The diagram below shows how the GKN/Melrose model produces exceptional margins relative to the margins produced by other syndicate members who are party to the RRSP (others typically have significantly higher costs):

Melrose estimates that the cash generated over the next 30 years through RRSPs will amount to approximately GBP £22 billion. The company refers to this as its "future cash mountain," which is the primary reason behind its strategic shift from a successful turnaround business to a dedicated aerospace company. This transition was deemed the most advantageous capital allocation option available.

The Engines division maintains a global presence, with its components featured in most commercial aircraft engines. Its RRSP portfolio includes partnerships with all major engine original equipment manufacturers (OEMs), covering 73% of flight hours for narrow-body aircraft and 68% for wide-body aircraft worldwide.

It currently has 19 RRSPs (each relating to a particular engine type), 17 of which are in the cash generative phase and two more will become cash flow positive in 2028.

Even better, Melrose's partnership share in RRSPs has grown in recent years. For the older CFM56-5/-7 engines, which power around 20,000 engines currently in service, Melrose's share was below 2%. With no new deliveries expected for this outdated technology, aircraft equipped with these engines will gradually be phased out.

Concurrently, the new Pratt & Whitney GTF engines feature RRSPs that provide Melrose with a significantly larger share of 4-7%. Currently, about 3,000 of these engines are in service, but future deliveries are projected to reach approximately 18,000.

Consequently, as the engines with lower revenue share phase out and the more of the engines with a higher revenue share deployed, Melrose's RRSP revenue stream will grow steadily. In fact, cash inflows from the RRSP portfolio are expected to increase each year until at least the 2050s.

The primary drawback of the RRSP model, which should be noted, occurs during the initial phase of introducing a new engine to the market - a challenge that Melrose currently faces.

If a manufacturing defect or minor design flaw is found in a part of the engine supplied by another company, cash flows under the RRSP are negatively impacted for all parties until the issue is resolved. Additionally, as risk is shared, all parties may be liable for some of the remedial costs, creating significant interdependencies.

Such setbacks are common when introducing new aerospace technologies. The complexity of modern engines means that unexpected issues are almost inevitable.

This situation is currently affecting the new geared turbofan engines developed by Pratt & Whitney, a division of RTX (formerly Raytheon Technologies). These engines, fitted on the Airbus A320neo family of aircraft, have encountered a powder metal manufacturing issue in the turbines of roughly half of the 1,360 geared turbofan-equipped A320neos currently in service. As a result, around 600-650 planes have been grounded worldwide in 2024. Airlines, including Lufthansa, are managing the disruption by extending the service life of older A320ceo aircraft and wet-leasing narrow-body planes from other carriers.

Repairing the Pratt & Whitney engines is a lengthy process, requiring 250-300 days per engine. Work will continue into 2026 until the affected aircraft are repaired and back in service. In respect of the grounded aircraft, no revenue will be generated under the RRSP in respect of service and maintenance of those engines until they are back in service. This will impact all stakeholders, including Melrose, which holds a 4% RRSP share for that engine.

Despite this matter being entirely beyond the control of Melrose, negative sentiment among short-term stock market investors has dampened demand for the shares and so contributed to the temporary dip in its share price.

As explained, resolution efforts by Pratt & Whitney are already well underway, with the repair program expected to cost USD $6 to $7 billion in total. Based on its 4% share, Melrose's estimated exposure is around GBP £200 million. However, the company has indicated that this will not affect its profitability, thanks to conservative early lifecycle assumptions that included contingencies for unforeseen costs.

As more grounded aircraft return to service over the next few years, Melrose's revenues are expected to improve significantly, leading to better financial results between now and 2026.

The grounding has also impacted Airbus's production targets, reducing expected jet deliveries for 2024 to approximately 770, down from a previously announced 800. Additionally, plans to ramp up production of the A320neo family to 75 jets per month have been postponed from 2026 to 2027. This means that in the short-term Melrose revenue generation will be slightly softer than would have otherwise been the case, but these planes will come in to service, so it should be seen as a delay to revenue rather than lost revenue.

Despite these challenges, demand for the new engines remains strong. They offer 16%-20% better fuel efficiency, leading to significant fuel savings and lower operating costs for airlines. The engines also reduce carbon emissions by 16%-20%, supporting airlines in meeting stricter emissions regulations and ESG objectives. Furthermore, they generate 75% less noise, improving the passenger experience and reducing noise pollution around airports. Consequently, airlines continue to support the new technology and are willing to wait for the current issues to be resolved.

In the Structures division, Melrose has taken steps to boost profitability by divesting low-margin assets, such as its defense structures business to Boeing, and focusing on high-value contracts, primarily with Airbus. Although this segment is not as lucrative as the Engines division, it still offers growth potential, particularly through the optimization of existing operations which will significantly expand margins.

Overall, Melrose’s engine and structural technologies are integrated into all major, high-volume aircraft platforms. The aerospace market is poised for long-term growth, supported by record aircraft order books, which bodes well for the company’s future prospects.

Growth

Melrose operates in a niche market dominated by a few major players, and its strong partnerships with leading engine manufacturers bolster its competitive position and create a solid foundation for growth.

The aerospace sector is rebounding as global air travel recovers from the COVID-19 pandemic, with flight hours now surpassing pre-pandemic levels. This resurgence, coupled with aging aircraft fleets, drives aftermarket growth in maintenance and servicing, from which Melrose benefits as an RRSP participant, earning a share of service fees even when other parties handle the actual maintenance.

Simultaneously, many airlines are modernizing their fleets, increasing demand for new, fuel-efficient, and environmentally friendly engines. This trend creates opportunities for Melrose to expand its RRSP revenue base with aircraft that will remain in service for at least 15-20 more years. In the first half of 2024, over 950 new engine orders were placed, contributing to a record backlog of approximately 15,000 civil aircraft orders, with delivery slots extending into the 2030s.

Looking ahead, two next-generation engines are under development:

An evolution of the current Pratt & Whitney GTF engine.

The CFM International RISE ("Revolutionary Innovation for Sustainable Engines"), an open rotor engine under development by CFM International, a joint venture between GE Aerospace and Safran Aircraft Engines. This engine is designed to support hydrogen and sustainable aviation fuels, aiming for a 20% reduction in fuel consumption and carbon emissions.

Melrose stands out as the only global player involved in both of these next-generation projects, positioning it for future success as new engine technologies are set to drive revenues and profitability for decades, creating durable future cash flows not yet reflected in its share price.

It is clear that new engine technology will drive revenues and profitability for decades to come, providing durable future cash flows that are not reflected in the current share price of Melrose.

Additionally, increased government defense spending due to geopolitical tensions and NATO's commitment to allocate 2% of GDP to defense has resulted in record defense order backlogs, providing another revenue stream for Melrose.

Melrose's competitive edge is further strengthened by GKN's expertise in Additive Fabrication (AF), a process that reduces costs, enhances output quality, and allows for greater design flexibility (see the short video below).

This advantage facilitated the expansion of its RRSP on the GEnx (General Electric Next-generation) dual rotor, axial flow, high-bypass turbofan engines.

GKN has been pioneering AF technology for over 20 years, boasting proprietary software and an unmatched data bank, and it is the only company with AF components currently in operational aircraft. Melrose is investing in the industrialization of AF technology, with a target internal rate of return (IRR) exceeding 20% for the project.

Management Team

The leadership team at Melrose possesses a profound understanding of the technical and operational facets of aerospace manufacturing and maintenance, which is vital for navigating this complex industry.

Peter Dilnot, appointed as Group CEO on March 6, 2024, brings significant expertise to the role. He previously led GKN Aerospace and has been a Melrose Executive Director since January 2021, following his tenure as Chief Operating Officer starting in April 2019. Dilnot's background is rooted in engineering and aviation, beginning his career as a helicopter pilot in the British Armed Forces. He holds a degree in Mechanical Engineering and has experience with the Boston Consulting Group, where he spent seven years, and with Danaher Corporation as a senior executive. His time at Danaher, renowned for its disciplined approach to corporate stewardship, cost management, and innovation, has influenced the strategic practices already evident at Melrose Industries.

“We remain confident of delivering on our 2024 and 2025 guidance; our positive outlook and disciplined capital allocation enables us to invest more in attractive organic growth opportunities, as well as continue shareholder returns through our growing dividend and the further share buyback programme announced today… We have made strong progress in the first half [of 2024], driven by Engines aftermarket performance and business improvement actions… We have positive momentum, a clear strategy and excellent growth opportunities ahead.”

Peter Dilnot, CEO, Melrose Industries

Financials

The company aims to significantly improve margins by 2025, with operating margins targeted to reach 28% in the Engines division (a 500 basis point increase from 2023) and 9% in the Structures division (a 600 basis point increase from 2023), resulting in a blended margin exceeding 18%.

")

“Our profit more than doubled in 2023, and is expected to expand significantly again to reach our 2025 targets. We will see increasingly higher drop through from the strong Engines division growth in the years ahead.“

Peter Dilnot, CEO, Melrose Industries

The first half of 2024 showed early signs of growth for Melrose, despite ongoing restructuring costs and challenges with Pratt & Whitney's new geared turbofan engines. Revenue rose by 6.7% to GBP £1.74 billion, with the Structures division contributing a 6% increase to GBP £1.02 billion, while the Engines division saw a 21% rise to GBP £720 million.

However, the pretax loss widened to GBP £105 million from GBP £62 million a year earlier, primarily due to industry-wide supply chain disruptions. These challenges are expected to persist into 2025, leading the company to revise its 2025 revenue guidance down to GBP £3.8 billion from the previous estimate of GBP £4.0 billion.

Despite these hurdles, the business is second half weighted in the Structures division and Melrose maintains a positive outlook for the second half of 2024, keeping its full-year revenue guidance at GBP £3.6 to £3.75 billion and adjusted operating profit projections at GBP £550 to £570 million - which you will note is more than double the figures for the first half.

The company's net debt stands at GBP £976 million, with a leverage ratio of 1.7x. Melrose ultimately aims to bring this ratio down to achieve investment-grade status, but in the short-term sets itself a range of 1.5x to 2.0x.

Growth investments are ongoing, including a new engines repair center in California and a GBP £50 million expansion of Additive Fabrication capacity in Sweden.

The majority of restructuring cash outflows are expected to conclude by the end of 2024, and in respect of CAPEX spending, depreciation and amortization expenses are far larger than ongoing capital expenditures, suggesting declining maintenance spending. Growth CAPEX will increase as investments are made to drive the business forward in meeting its very ambitious expansion objectives - particularly around the unique opportunity to grow the Additive Fabrication technology that the business has pioneered (anticipated to yield >20% IRR).

From 2025, Melrose anticipates double-digit EPS growth and a significant increase in free cash flow, projecting 80-85% cash conversion from its expanding Structures segment and non-RRSP Engine businesses.

The only criticism of the stewardship of this business relates to its insistence on paying a progressive dividend, regardless of circumstances. This is a very British/European thing and it makes little or no sense. While Melrose has shown willingness to repurchase shares when feasible, paying dividends during a period of negative net earnings is illogical on two grounds. First, it involves borrowing or distributing balance sheet assets to satisfy income-seeking investors. Second, with a dividend yield of just 1.9%, this approach is unlikely to appeal to income investors who are easily able to achieve higher yielding assets elsewhere. At the same time this dogmatic commitment to dividends frustrates those who prefer capital to be allocated for debt reduction or share buybacks of undervalued stock. As such, the progressive dividend policy seems to satisfy none of the company’s shareholder base! (For a better understanding of why dividends are the wrong choice for Melrose, please read this explanation).

Is Melrose Industries A Good Investment?

You will recall from the beginning of this report that the GKN Aerospace business was so compelling to insiders at Melrose Industries, that not only did they aggressively acquire it, but they abandoned their previous very successful business-turnaround model in order to go all-in on this opportunity. That in itself is incredibly compelling.

I hope that this investment thesis has explained why the Melrose Industries management is so excited about the future prospects of this business.

To date the market has been hesitant to fully recognize Melrose Industries’ potential, partly due to uncertainties related to GKN's acquisition and subsequent restructuring, and partly due to the setbacks with the Pratt & Whitney geared turbo-fan engine.

As Melrose Industries continues to deliver on its strategy and demonstrate the financial benefits of its streamlined operations, investor sentiment is likely to improve.

Melrose's business model generates significant cash flow, with long-term visibility due to the contractual nature of its RRSPs. The company’s engine contracts are underpinned by robust demand for aircraft maintenance and spare parts, with cash flow projections extending into the 2060s. This consistent revenue generation will enable Melrose to pursue aggressive share buybacks, currently targeting 5-10% of outstanding shares annually, which will enhance shareholder value significantly over time. Melrose completed a GBP £500m share buy-back programme in September 2024, and announce another GBP £250m of buy-backs to take place before March 2026.

Melrose’s aftermarket services for engines provide higher margins compared to initial production. As flight hours increase and aircraft fleets expand, the need for engine overhauls and part replacements will likely grow, boosting Melrose’s profitability. The company’s business model, which capitalizes on the high-margin aftermarket rather than low-margin OEM sales, positions it favorably for long-term gains.

As the aerospace industry evolves, Melrose is well-positioned to benefit from advancements in engine technology, such as the shift towards geared turbofan engines and future developments in sustainable aviation including hydrogen powered aircraft. Its focus on structural components in engines ensures that Melrose remains a key player in next-generation propulsion technologies without the high risks associated with manufacturing complex rotating parts.

The company is currently trading on a forward single-digit earnings multiple, which seems crazy given that this is a business enjoys a wide moat, strong operating leverage, impressive margins that are still expanding, and durable earnings for decades to come.

However, Melrose's financial performance is heavily tied to the success of its RRSPs with major engine manufacturers. Any setbacks in engine production or design flaws, as seen with Pratt & Whitney's geared turbofan turbine blade issues, can delay revenue recognition and impact cash flow. While Melrose's strategy mitigates direct exposure to these issues, they can still affect the broader aerospace supply chain and slow cash flow realization.

The aerospace sector is also inherently cyclical, with demand for aircraft fluctuating based on global economic conditions, fuel prices, and travel trends. While current market conditions favour growth, any significant downturn could result in reduced orders for new aircraft and deferred maintenance, negatively impacting Melrose's revenue.

In conclusion, Melrose represents a compelling investment opportunity in the aerospace sector. Its successful restructuring from a diversified industrial conglomerate to a streamlined aerospace player has unlocked significant value. The company's focus on long-term, high-margin cash flows from engine services, backed by a strong leadership team and strategic share buybacks, offers a solid foundation for future growth. Multiple expansion will occur as the market wakes up to this very rare long-term investment opportunity which will appeal to buy-and-hold investors focused on long-term uninterrupted compounding.

There are four fundamental drivers of shareholder returns: increasing revenue, improving margins, valuation multiple expansion and a contraction in the number of shares outstanding (contrary to popular opinion, dividends do not feature in this list as they often destroy shareholder value, see here). Melrose has all four of these key drivers and these have a multiplicative effect on investment returns.

Valuation on this kind of opportunity is inherently subjective, and forming your own opinion is key. However, in some cases, investment opportunities are so clearly favorable that precise valuation isn't even necessary. As Charlie Munger once said, "If you see a fat man walking down the street, you don’t need to weigh him to know that he’s fat." This metaphor captures the way in which Munger invested, and it seems perfectly apt with Melrose Industries.

Melrose Industries Investor Presentation

You are encouraged to watch this video after having read the analysis above. It will likely answer any further questions that you may have. Pre-reading of the analysis is recommended as it provides the requisite context and the depth of understanding to assimilate the information provided in this presentation.

Melrose Industries - Trading update 6th March 2025

The company reported annual profits at the top-end of expectations, and raised its dividend by a fifth.

For the year to 31 December 2024, revenue was up 6 per cent to £3.5bn on engines segment growth of over a quarter. Adjusted operating profit rose 42 per cent to £540mn.

Management anticipates some potential volatility in the year ahead due to geopolitical pressures, but sees these as no more than short-term headwinds that will soon abate. However, the short-termism of the market has seen the shares marked down today on this note - maybe another buying opportunity?

The investment thesis is still very much in place and long-term growth lies ahead. The company set out new five-year targets for annual revenue of around £5bn, adjusted operating profit of at least £1.2bn and free cash flow after interest and tax of £600mn.

In terms of operating profit, if these targets are achieved, we are looking at 17.3% CAGR over the next 5 years. I would be happy with that, yet these targets are almost certainly conservative, so achieving more is likely. This is a robust business with a unique business model and some core commercial advantages (read the full analysis to understand more).

The market reaction following the the Trading Update yesterday looks over done.

Summary of the earnings call:

1. Positives for Melrose Industries PLC

Strong Financial Performance in 2024

- Profit at the top end of expectations despite industry challenges

- 42% increase in profit to £500 million

- 11% revenue growth on a like-for-like basis, led by the Engines division

- Margins continued to grow, up 400 basis points to 15.6%

- Earnings per share (EPS) grew significantly, up 45% to 26.4p

Engines Division Performance

- Engines revenue grew 26%, driven by strong aftermarket performance

- Aftermarket revenue was up 32%, with particularly strong performance in the Swedish military business

- Engines operating profit grew 40% to £290 million, and margins beat the 2025 target of 28% one year early at 28.9%

Structures Division Progress

- Margins continued to improve, growing from 5.1% to 7.2%

- Operating profit grew by 32% to £70 million

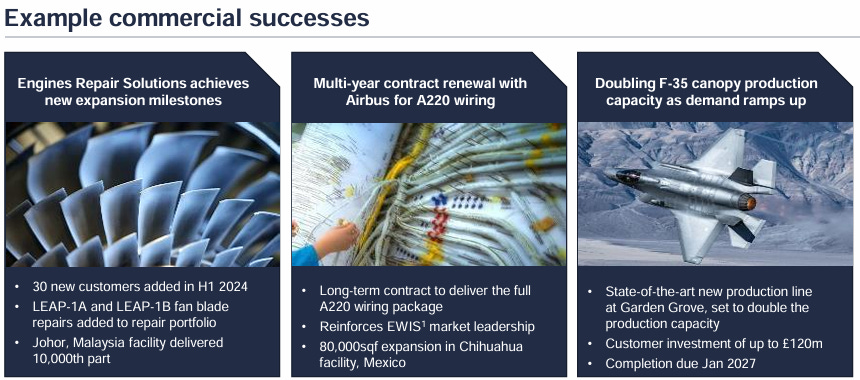

- Secured a contract renewal with Airbus for the full wiring package for the A220

- Secured customer investment of over £100 million to double F-35 Canopy production capacity

Future Outlook

- Positive momentum into 2025, with another step-up in profit and margins expected

- Extensive restructuring program to be completed in 2025, delivering improved productivity

- Reaching an inflection point on cash, moving from cash outflow in 2024 to over £100 million positive free cash flow in 2025

- Confident in achieving the 5-year targets set out two years ago

- Europe ramping up defense spending means that the military division of Melrose is highly likely to benefit.

2. Negatives for Melrose Industries PLC

Revenue Shortfall

- Overall revenue fell slightly short of expectations, primarily due to supply chain challenges and customer destocking in the Structures division - but revenue was still up 11% and margins improved

- Weaker dollar impact of around £30 million also contributed to the revenue shortfall - this is beyond the control of the company and invariably mean reverting over time

Structures Division Challenges

- Structures division revenue growth was dampened by ongoing supply chain challenges and customer destocking/production rate changes. In response, Melrose is employing a more capital-light approach to expanding its Structures business. For example, in the case of the F-35 Canopy program, Melrose secured funding from the U.S. Government and its customer Lockheed Martin to build a factory to double its production capacity, rather than using its own capital upfront. Concurrently, Melrose has been exiting businesses in the Structures division that are non-core and not profitable, in order to focus on a more streamlined and higher-margin portfolio.

Melrose's Additive Fabrication technology is a strategic priority for the company as it aims to address critical supply chain challenges in the aerospace industry, reduce costs and lead times, and improve the sustainability of its manufacturing processes. It's a a "revolutionary new way to manufacture structural components". The technology enables Melrose to "replace very expensive castings and forgings by thin metal structures with key features built on through Additive." This can deliver a "70% reduction in overall material use" and "substantial lead time reduction." Melrose has a clear roadmap to generate millions in incremental profit by 2029 through the commercialization and scaling of its Additive Fabrication technology.

Inventory Days Improvement

- Inventory days improvement is likely to come through in 2027-2029, as the supply chain stabilizes and the business ramps up. As Melrose's business continues to ramp up, the company expects to gain more predictability in its factories and manufacturing processes. This increased predictability and operational efficiency will allow Melrose to further optimize its inventory levels and drive down inventory days. It is shifting its focus from restructuring to "continuous improvement" initiatives, which include using lean manufacturing approaches and operational efficiency programs.