SoftwareOne Holdings

A Turnaround In The Cloud

DISCLAIMER & DISCLOSURE: The author has a position in SoftwareOne at the time of publication, but that may change. The views expressed are those of the author at the time of publication and may change without notice. The author has no duty or obligation to update this information. Some content is sourced from third parties believed to be reliable, but accuracy is not guaranteed. Forward-looking statements involve assumptions, risks, and uncertainties, meaning actual outcomes may differ from those envisaged in this analysis. Past performance is not indicative of future results. All investments carry risk, including financial loss. This analysis is for educational purposes only and does not constitute investment advice or recommendations of any kind. Conduct your own research and seek professional advice before investing.

Microsoft’s Most Important Channel Partner

In the vast landscape of enterprise technology, trillion-dollar platform companies like Microsoft, AWS, Salesforce and Adobe face an immense logistical challenge. They need to connect with hundreds of millions of businesses that rely on their software and services, but it’s simply impossible for these giants to maintain direct relationships with every end user.

On the other side, the average enterprise isn’t a technology expert. Most rely on a patchwork of vendors supplying HR systems, payroll software, CRM platforms, cybersecurity tools, workflow systems, advertising portals, cloud services and more.

Somewhere between these two worlds sits a crucial but often overlooked layer of the tech economy: the channel partner experts that bridge the gap between complex software ecosystems and real-world business needs.

Channel partners are far more than just outsourced sales teams. Yes, they help big software vendors reach more customers, but their role runs much deeper. They nurture client relationships, guide businesses through continual modernization requirements and ensure that complex software ecosystems actually deliver value. From implementation and customization to ongoing service management, they act as trusted advisors. They also help with risk mitigation, covering everything from compliance and license optimization to security and disaster recovery. Ultimately, they help clients sharpen their IT spending, extract more value from their technology stack, and improve efficiency. For many enterprises, these partners become indispensable allies.

At the forefront of this ecosystem stands SoftwareOne Holding AG (Switzerland: SWON). You might not have heard of it, but it happens to be Microsoft’s largest channel partner. Scale alone makes SoftwareOne impressive, but what truly sets it apart is its strategic importance in a world where artificial intelligence is transforming how technology is built, sold and used.

SoftwareOne’s business model has several structural advantages that make it uniquely appealing. It’s a business which demonstrates tollbooth-like characteristics, earning recurring economic rents by sitting between enterprise customers and major technology vendors. As software products constantly evolve, SoftwareOne’s role as an expert navigator of this complexity becomes even more valuable. Its technical know-how and deep customer relationships create a renewable stream of opportunities and revenue.

More specifically, the company’s strengths include:

It’s capital-light: no warehouses, no inventory, no R&D, and minimal capex, making it easy to scale globally.

It owns the customer relationship, giving it sticky recurring revenues as software and cloud consumption continue to grow, especially in the AI-driven cloud era.

Many of its large customers engage in multi-year licensing agreements and renewals creating an annuity-like revenue base (though at times with variability in timing).

It converts profits into cash efficiently, with customers typically paying upfront.

It benefits from favourable working capital dynamics and channel partner incentives, as major software vendors spend billions each year supporting their partners.

And finally, with companies spending around 8% of their revenue on IT services, SoftwareOne’s addressable market is enormous.

So, now that you understand why it is a great business, what makes it compelling as an investment today?

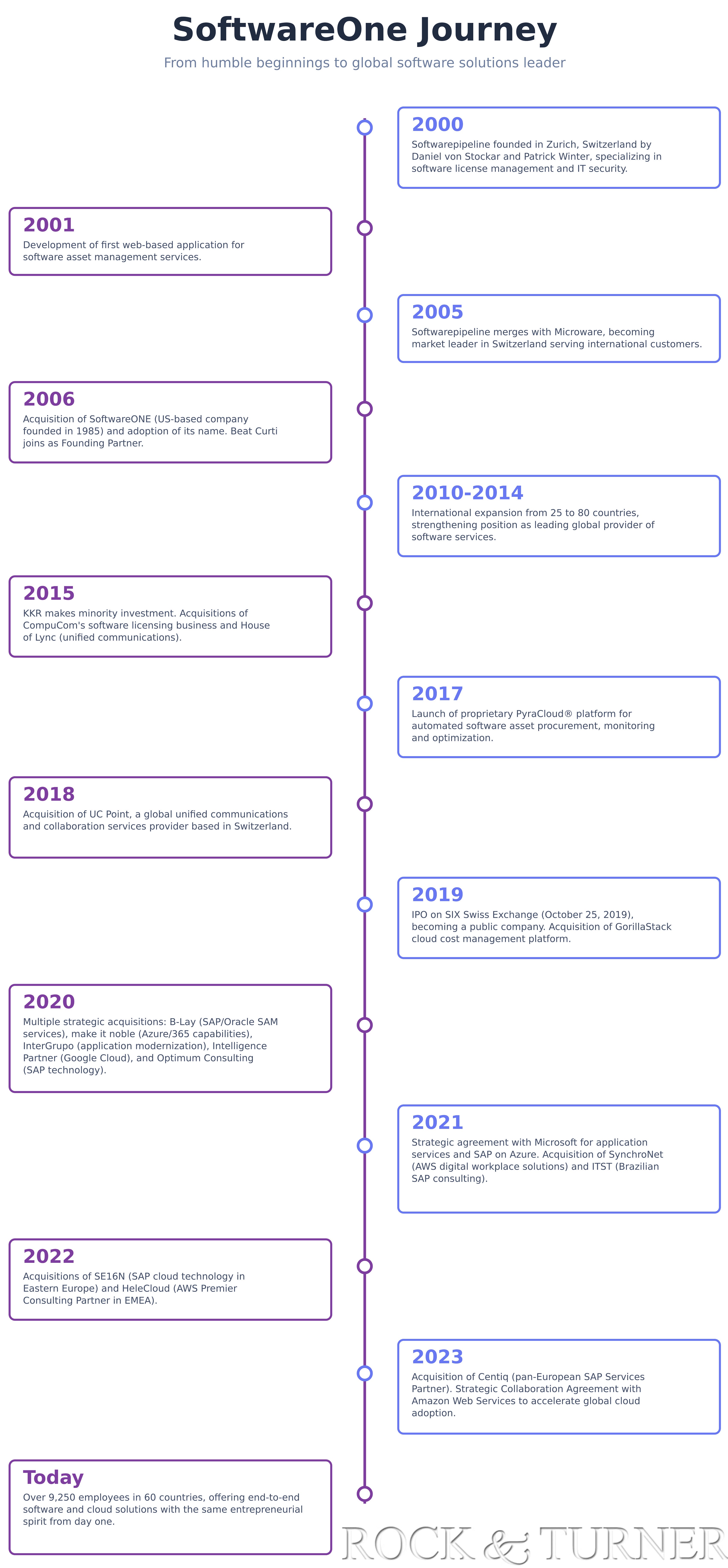

Founded in 2000, SoftwareOne spent nearly 25 years building dominance as Microsoft’s largest channel partner. But in recent years, it hit turbulence: some, but not all of it self-inflicted. This caused its share price collapse.

Market psychology tends to overshoot in both directions, and SoftwareOne now looks too heavily oversold. That creates an intriguing asymmetric risk/reward opportunity.

The internal missteps that once dragged on performance have largely been fixed with a complete change of management. Additionally, external headwinds are turning into tailwinds. Last, but by no means least, recent M&A activity appears set to strengthen the business further, improving both its competitive position and unit economics.

While I don’t usually focus on special situation investing opportunities, SoftwareOne is an exception that caught my attention. It’s a business with solid fundamentals, improving momentum and a valuation that looks too good to ignore.

Understanding Digital Distribution

The rise of SoftwareOne is told in a chapter of the evolution of enterprise IT itself: a story that begins long before the cloud, long before Microsoft or AWS, and long before software became invisible yet indispensable.

In 1954, Remington Rand installed the world’s first commercial business computer (the UNIVAC I) at General Electric. It was a behemoth of a machine, filling an entire warehouse and costing the equivalent of $20 million in today’s money. Back then, relationships between technology vendors and customers were intensely direct and painfully complex. It took teams from Arthur Andersen, General Electric and Remington Rand nearly three years just to deliver a functioning payroll program.

The next chapter arrived with IBM’s mainframe era. IBM created what became known as “walled gardens,” where buying IBM hardware meant locking yourself into IBM services, IBM software, and, inevitably, more IBM hardware. This vertically integrated model was immensely profitable, but also suffocatingly closed.

That began to change when the U.S. Department of Justice filed an antitrust lawsuit against IBM, forcing it to dismantle its monopoly and open its architecture. In an ironic twist of history, IBM outsourced parts of its software development, including the operating system for its new personal computers, to a tiny startup run by two precociously talented young programmers. One of them was Bill Gates. That decision gave birth to Microsoft and changed the trajectory of the technology industry forever.

When IBM launched its first Personal Computer (PC) in the early 1980s, it was built on open architecture and standardized components: an Intel x86 processor, Microsoft’s MS-DOS operating system and universally compatible interfaces. The result was explosive. Competitors like Dell, Hewlett-Packard and Compaq began producing “IBM clones,” ushering in an era of standardization that shattered the dominance of proprietary systems.

This transformation fundamentally rewired the IT landscape. Software could now be written for portable standards rather than bespoke architectures. Independent software vendors flourished and a new generation of programmers realized they could build applications that scaled across diverse hardware environments.

But with opportunity came complexity. As IT estates became more fragmented and heterogeneous, businesses found themselves overwhelmed. They needed experts who could make sense of the expanding ecosystem, integrate disparate technologies and translate vendor offerings into real business outcomes.

That demand gave birth to a new breed of intermediary. Broadline hardware distributors such as Tech Data (founded in 1974), Ingram Micro (1979) and Synnex (1980) emerged as the backbone of enterprise IT logistics. Soon after came the value-added resellers (VARs) and IT solution providers like CDW (1984) and SHI (1989), who didn’t just sell products, they helped implement, customize and support them.

Decades later, the cloud has reshaped how technology is delivered, but not the need for intermediaries. If anything, that need has grown stronger. Global IT spending now exceeds $5 trillion annually and over 70% of it flows through channel partners. Their role as translators, integrators and trusted advisors remains just as vital today as it was when the first mainframes came online, perhaps even more so in a world where AI, cloud, and data complexity define the modern enterprise.

The Genesis of SoftwareOne

Founded in Zurich in 2000 by Daniel von Stockar and Patrick Winter under the name Software-Pipeline, SoftwareOne began as a pioneer in software asset management. This was a niche but vital corner of the tech world focused on helping businesses manage, license and optimize their growing software portfolios. From those early days, it expanded rapidly, evolving into a truly global organization that now serves more than 200,000 customers across 70 countries.

Even after going public, the founders remain deeply invested, collectively holding more than 20% of the company’s outstanding stock. That’s not the behaviour of short-term opportunists. These are missionaries - leaders who care about building enduring value, not just cashing out. It’s an important detail and one we’ll come back to later, because founder alignment often proves critical in the long-term trajectory of a business like this.

Today, SoftwareOne operates two main segments: (1) Software & Cloud Marketplace, which comprises software license reselling and cloud subscriptions, and (2) Software & Cloud Services, which includes value-added IT consulting, implementation, and managed services around those software solutions

It processes annual gross billings exceeding CHF 25 billion (~$31 billion U.S. dollars) and has earned the distinction of being Microsoft’s largest global channel partner. It’s a remarkable achievement for a company that started as a niche software advisory firm in Switzerland just a quarter of a century ago.

The growth has been extraordinary. Over the past decade, on a per-share basis, SoftwareOne has tripled its revenue and increased profits fivefold.

But as every good investor knows, no story is without its rough chapters. SoftwareOne’s journey hasn’t been entirely smooth and the turbulence it faced in recent years lies at the heart of why this investment story is so compelling. Let’s dig into that next.

The Technocrats, the Resistance & the Transformation

In 2018, tragedy struck SoftwareOne when its inspirational co-founder and CEO, Patrick Winter, passed away unexpectedly.

Winter wasn’t just a leader, he was the company’s cultural heartbeat. Beloved by employees and respected across the industry, he had taken SoftwareOne from a small Swiss startup to a global powerhouse serving over forty thousand corporate clients. Under his leadership, the company had grown revenue by 29% annually for a decade and expanded EBITDA thirty-four-fold. His death left a leadership void at the very moment SoftwareOne was preparing for its IPO and finalizing its largest-ever acquisition, Comparex.

Stepping into that vacuum was Dieter Schlosser, the company’s COO, who led SoftwareOne through its 2019 IPO and the uncharted territory of the pandemic years. As a newly public company, corporate governance reforms required the board to transition to a majority of independent directors - technocrats with strong résumés but little or no personal investment in the business. At this stage, only one founder remained on the board: Daniel von Stockar, serving as chairman.

The pandemic proved a difficult test. Many of SoftwareOne’s customers froze spending and conserved cash, cutting back on IT budgets just as SoftwareOne was expected to deliver growth. Results disappointed. By late 2022, the board asked von Stockar to step down and he resigned in April 2023.

Then came a search for a new CEO. Contrary to the practice of SoftwareOne, which had always been to promote from within so that its unique culture could be preserved, the board appointed Brian Duffy, an outsider and first-time public company CEO who happened to have 17 years of experience at Microsoft. Backed by the board, Duffy then began reshaping the leadership team, pushing out several long-serving executives who had been with SoftwareOne since its early days.

Members of the founding group, comprising von Stockar, René Gilli and Beat Curti, still owned approximately 29% of the company and became rightfully concerned. They were watching a board with little personal stake dismantle the culture they’d built and systematically destroy the very ethos that had made SoftwareOne successful. So they decided to act.

In June 2023, not long after Duffy officially took the helm, the founding group and Bain Capital partnered to make a take-private offer of CHF 18.50 per share. To put this in context, it was about 12x trailing EBITDA and a 33% premium to the prevailing market price. The board rejected the proposal, calling it too low. Over the following months, the founders and Bain raised their bids up to a ceiling of CHF 20.50 per share, but the board continued to refuse without ever putting the offers to a shareholder vote.

Then came the breaking point. On October 31, 2023, SoftwareOne announced it had been blindsided by changes to Microsoft’s incentive structures, a stunning oversight given its 30-year history of managing such transitions smoothly. The company issued a profit warning, cutting EBITDA guidance by 15%, or roughly CHF 40 million. The stock plummeted more than 40% in a single day, wiping out CHF 860 million in market capitalization.

By February 2024, the founders had had enough. They called for an extraordinary general meeting to replace the board entirely and by April, they succeeded in regaining control.

Unfortunately, damage had been done. SoftwareOne’s thirty-year track record of managing Microsoft incentive changes through proactive relationship management had been neglected by incumbent leadership focused on corporate processes rather than customer and vendor needs. Simultaneously, the new go-to-market sales motion was rolling out in Q2, with rushed implementation causing some customer disruption and account manager changes in regions like North America.

The founders moved quickly to stabilize the business. Duffy was removed as CEO, and Raphael Erb, who had joined SoftwareOne aged 19, and spent more than 25 years with the firm, was appointed as his successor. Erb had most recently led the Asia Pacific region, the company’s fastest-growing division, consistently delivering double-digit growth into 2025. He was a cultural fit, a proven operator and the right leader to restore the company’s entrepreneurial DNA.

Erb wasted no time. He appointed new regional heads for DACH (Germany, Austria, Switzerland) and rEMEA (Rest of Europe, Middle East, and Africa), and promoted SoftwareOne veteran Oliver Berchtold to President of Software and Cloud. Together, this refreshed leadership team averaged nearly 17 years of tenure, a powerful signal of continuity and experience: restoration of the original corporate culture.

Erb then launched a sweeping decentralization plan to restore agility. The idea was simple: eliminate unnecessary management layers and push decision-making and P&L responsibility down to the 60-plus country organizations closest to customers. The program targeted CHF 50 million in cost savings but overdelivered early, achieving a run-rate saving of CHF 88 million.

Then, less than two months into Erb’s tenure, came a bold and surprising move. On December 19, 2024, SoftwareOne announced the acquisition of heavy-weight competitor Crayon Group, a Nordic software and cloud solutions company, and Microsoft’s fifth-largest global channel partner.

Strategically, the fit was elegant. Both companies shared capital-light business models centered on software asset management and value-added services. Their geographic footprints were complementary: Crayon dominated the Nordics and small-to-midsize client base, while SoftwareOne was strong in the DACH region and large enterprises. Together, they would serve over 200,000 customers across 70 countries, cementing their position as Microsoft’s largest and most capable channel partner.

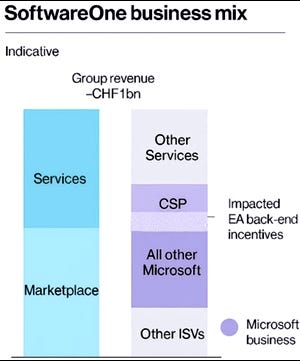

SoftwareOne’s revenues are primarily driven by global enterprise IT spending on software licenses and cloud subscriptions. In the midst of the AI revolution, who wouldn’t want to be operating in that space? But it’s better than simply operating in the right segment of the market, the graphic below shows where SoftwareOne and Crayon fit in the Microsoft ecosystem. These two companies are arguably not only in the best place, but now they are one business, so they own that part of Microsoft’s eco-system.

Yet the initial market reaction was negative, let me explain why and then let’s dive deep into what makes this business special following the acquisition and management shake up before breaking down the valuation to answer the ultimate question of whether SoftwareOne is a good investment today.

SoftwareOne paid NOK 13.5 billion (CHF ~1.1 billion) for Crayon, which had generated NOK 1.17 billion (CHF ~93 million) in EBITDA in 2024. On paper, that implied roughly a 11.5x multiple, reasonable given Crayon’s 27% EBITDA growth that year, its expectation of 20%+ growth in 2025, not to mention its excellent cash flow conversion.

The issue wasn’t really the price, it was the perception: SoftwareOne itself, trading at depressed levels following its period of turbulence, was valued by the market at a similar CHF 1 billion despite producing CHF 223 million in EBITDA. The question being asked by the market was how could both businesses be valued at the same level? To make matters worse, SoftwareOne paid half of the acquisition price with its own undervalued stock, which only amplified investor skepticism. Why swap a share of CHF 223 million in EBITDA for the same proportional share of CHF 93 million?

But the market reaction missed the bigger picture. SoftwareOne’s depressed share price made it a poor benchmark for valuation. Crayon was growing faster, enjoyed superior margins through its focus on Microsoft’s high-value CSP program and had built deep AI expertise over a decade. These were traits that warranted a premium. Beyond that, the merger’s synergy potential was substantial.

SoftwareOne expects CHF 80–100 million in cost synergies from consolidating sub-scale geographies, integrating back-office operations and streamlining management layers. The merger should also improve quality and performance, especially in North America, where Crayon’s operational strength can re-energize SoftwareOne’s underperforming business.

Beyond the cost synergies, there is also enhanced revenue to factor in to analysis. Although these are harder to quantify, they could be meaningful. Cross-selling, enhanced service portfolios and broader access to enterprise accounts could add another CHF 50 million to EBITDA - not an unreasonable assumption based on past integration outcomes. All told, the merger could drive 40% profit-per-share growth over the next two years, before even accounting for organic momentum.

Crucially, the deal was financed prudently. The cash portion came from low-cost credit facilities at less than 1% interest (SARON + 0.85%), leaving the transaction roughly EBITDA-multiple-neutral after synergies and more than 20% accretive to free cash flow per share.

Following the acquisition of Crayon, the company created a co-CEO structure, with Melissa Hulholland, formerly CEO of Crayon, joining Raphael Erb to lead the business.

Erb (Swiss national) oversees activities in the regions as well as Services and Marketplace, with all Regional Presidents reporting to him directly. Mulholland (U.S. national) leads strategy, customer platforms, GTM enablement, vendor alliances and global functions including people & culture, finance, marketing, communications, M&A, legal, and IT. Of note is that Mulholland joined Crayon after a distinguished 12-year career at Microsoft where she led the global strategy and business development. The SoftwareOne leadership team is now super-strong.

Together, SoftwareOne and Crayon form a formidable platform: financially stronger, operationally leaner and strategically positioned at the crossroads of AI, cloud and enterprise modernization. Both companies bring deep acquisition experience, having collectively completed more than two dozen M&A transactions, suggesting further industry consolidation could lie ahead.

This is supported by strategic growth initiatives (such as Vision 2026) which include:

Deepening hyperscaler partnerships (Microsoft, AWS, Google) to drive higher customer cloud consumption. For instance, SoftwareOne was an early partner in rolling out Microsoft’s Copilot AI and sees ~CHF 100m mid-term revenue opportunity in AI-enabled cloud services;

Scaling data and AI solutions leveraging its “Intelligence Fabric” offerings and analytics expertise to capitalize on the fast-growing demand in data analytics and AI;

A focused ISV strategy – concentrating on key independent software vendors beyond Microsoft (Adobe, Oracle, VMware, SAP, and a long tail of others) with dedicated teams, to capture more wallet share from these channels;

SoftwareOne is investing in its self-service portal as a one-stop digital marketplace for clients, aiming to raise the growth rate of its Marketplace business from a historical ~9% to ~15% CAGR by 2026, Mmore on this later, suffice it to say that this portal, along with software lifecycle management tools, should improve customer retention and sales efficiency by providing a unified platform for procurement and spend management;

Targeted bolt-on M&A.

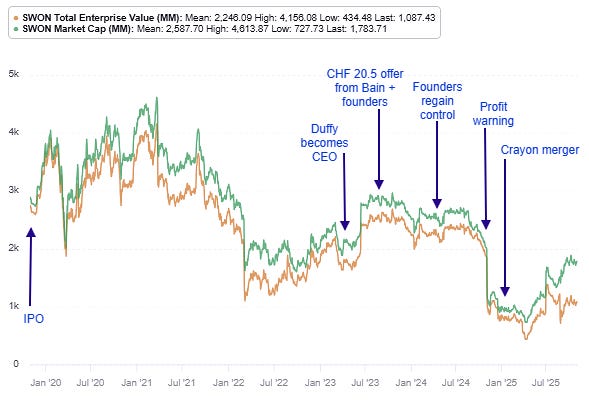

After years of turbulence, SoftwareOne has emerged bigger, more focused and better led than ever before. Yet the market hasn’t fully caught up to that reality. Its valuation remains deeply discounted, creating a rare opportunity where perception and fundamentals are misaligned.

The company is bigger and stronger than ever before and yet the market cap and enterprise value are at lows:

Although SoftwareOne’s primary listing is on the SIX Swiss Exchange, following the Crayon acquisition it now has a secondary listing on the Oslo Stock Exchange, opening up new liquidity pools for its stock. It shouldn’t take too long before a re-rating occurs.

To better understand just how compelling this business truly is, it’s worth looking a little deeper into what makes SoftwareOne so special.

The Competitive Landscape

To appreciate the unique position SoftwareOne occupies today, it helps to step back and look at the environment in which the company operates.

At one end of the spectrum are the pure-play distributors like Ingram Micro. These companies run capital-intensive operations with sprawling warehouse networks, billions of dollars tied up in inventory, and razor-thin gross margins earned on enormous transaction volumes. Their role is primarily wholesale: they move hardware and software at scale to value-added resellers (VARs) and systems integrators but offer limited solutions capabilities themselves.

VARs, on the other hand, such as CDW, add a layer of services on top of hardware sales: installation, configuration or device-attached support. This lets them earn higher margins than distributors, but it also anchors them to hardware-centric business models that are inherently regional. VARs typically specialize by geography or industry because their model doesn’t scale globally. That’s why, even today, there are no truly global VARs.

At the opposite end of the spectrum are the global systems integrators: names like Accenture, Tata Consultancy Services and Wipro. These firms are hardware-agnostic and operate at the high end of the IT value chain, managing complex, enterprise-scale transformations. They command high gross margins through consulting and professional services but earn little from product resale. Their models differ slightly: consultancy-led integrators like Accenture focus on strategic advisory and transformation, while delivery-led players like TCS and Wipro specialize in large-scale staff augmentation and managed services.

SoftwareOne sits squarely, and deliberately, in the strategic middle ground. Its positioning isn’t an accident but the result of conscious choices made decades ago. Unlike distributors, SoftwareOne works directly with end customers, building deep relationships and delivering high-value services. Unlike VARs, its early specialization in software licensing and related services made it capital-light and globally scalable from the outset. And unlike the big systems integrators, it generates substantial recurring revenue from licensing margins while building deep technical capabilities in key solution areas.

Its decisions have proven remarkably prescient, particularly in the age of cloud migration and AI evolution. The company’s focus has always been on the increasingly complex realm of software procurement, compliance and optimization, areas that became even more critical as public cloud adoption accelerated. As enterprises shifted workloads to platforms like Microsoft Azure and AWS, SoftwareOne captured that growth through its role as a reseller of cloud consumption, effectively monetizing infrastructure spending without the drag of owning any physical hardware or legacy distribution assets.

This unique positioning makes SoftwareOne mission-critical to technology vendors like Microsoft in a way few other partners can match. It results in an entrenched position that means disruption is highly unlikely leading to durable strong recurring earnings.

Although it works with many software providers, Microsoft is a major part of SoftwareOne’s revenues:

Should we be worried about customer concentration risk? In a word: ‘no’.

It’s important to understand where the exposure actually lies. Microsoft isn’t SoftwareOne’s customer; it’s the upstream supplier, the foundational technology partner whose products SoftwareOne helps bring to market. The real customers are the hundreds of thousands of organizations across the globe that rely on SoftwareOne to manage, optimize, and modernize their software estates.

With a customer base that broad and diversified, concentration risk is effectively diffused. What exists instead is a symbiotic relationship between the two businesses, each amplifying the other’s reach and relevance. Microsoft depends on SoftwareOne to help enterprises adopt and consume its technologies efficiently, while SoftwareOne’s success is anchored in the continued innovation and dominance of Microsoft’s software ecosystem.

That’s not dependency, it’s harmony.

Let’s take a closer look.

Microsoft’s Dependence on Distribution

Microsoft’s relationship with its partner ecosystem isn’t a matter of choice, it’s structural and indispensable to the company’s global reach. Roughly 95% of Microsoft’s total sales flow through its partner network, an ecosystem encompassing more than half a million firms worldwide.

This channel-based model enables Microsoft to serve every kind of customer, from Fortune 100 enterprises to local small businesses, without needing to manage the vast and costly direct sales, implementation and support infrastructure such coverage would otherwise demand. It’s a system designed for scale, efficiency and adaptability.

The economics are mutually beneficial. Microsoft invests billions of dollars each year in its partner incentive programs, creating a finely tuned framework of rewards that covers everything from transaction-based margins and solution delivery bonuses to marketing funds and enhanced payouts in strategic growth areas. For partners like SoftwareOne, these incentives, combined with front-end margins and recurring services revenue, form the foundation of a sustainable business model built around helping clients adopt, integrate and maximize Microsoft technologies.

But the partnership runs deeper than economics. Microsoft relies on its channel not just to sell, but to deliver expertise: specialized, domain-specific and localized capabilities that the company simply cannot maintain internally across every geography, vertical and customer type.

Consider a real-world example: a global manufacturer migrating from dozens of legacy ERP systems to a unified SAP S/4HANA platform hosted on Microsoft Azure. The project requires years of work, involving intricate cloud architecture design, data migration, application integration, custom development, user training and go-live support. Hundreds of skilled professionals must collaborate across time zones and disciplines. Microsoft cannot possibly deliver that depth of service alone. it needs partners like SoftwareOne to execute these transformations at scale.

Over time, Microsoft’s incentive structure has evolved in lockstep with its broader strategic priorities. Each shift in how partners earn reflects the company’s next stage of technological and business focus.

In the 1990s, software was still a physical product, sold on floppy disk or pre-installed on devices. Partners earned straightforward margins on license sales. The model was purely transactional: sell, ship and move on.

By the early 2000s, as hosting providers began offering “software as a service” (SaaS), Microsoft introduced the Service Provider License Agreement (SPLA). This was its first foray into recurring, usage-based licensing, an early glimpse of the subscription model that would later dominate.

Then came Azure in 2010 and Office 365, marking a seismic shift toward cloud computing. Microsoft began redirecting incentives away from on-premise products, rewarding partners for driving adoption of its cloud ecosystem instead.

The Cloud Solution Provider (CSP) program, launched in 2015, accelerated this transformation. It allowed partners to bundle Microsoft’s cloud offerings with their own managed services, creating deeper, more consultative customer relationships. Crucially, it also set higher competency requirements, pushing partners to evolve from simple resellers into trusted advisors.

The latest chapter came in 2024, when Microsoft overhauled its incentive structure again - this was the event that triggered the SoftwareOne profit warning.

To better understand what happened, first it is important to understand the various service options available.

For two decades, Enterprise Agreements (EAs) were the backbone of Microsoft’s enterprise ecosystem. These three-year contracts allowed large organizations, typically those with at least five hundred users, to lock in minimum license volumes in exchange for discounts and predictable pricing. Customers usually paid annually, but SoftwareOne earned most of its margin upfront, collecting incentive fees immediately upon contract signing.

EA reselling operated through two models. In the direct sales model, SoftwareOne acted purely as an advisor, with contracts and payments flowing directly between client and Microsoft. This structure, common among large enterprises, accounted for nearly half of Microsoft volume but delivered lower margins for SoftwareOne. In the indirect model, SoftwareOne managed the entire transaction, earning both front-end margins from pricing spreads and back-end rebates from Microsoft. This approach was significantly more profitable, giving SoftwareOne greater control and customer intimacy.

The Cloud Solution Provider (CSP) program now defines the future. Unlike the fixed-term EAs of the past, CSP offers flexible, evergreen cloud subscriptions with digital procurement and monthly billing. Within this framework, SoftwareOne runs two complementary models.

In the direct CSP business, SoftwareOne works directly with end users, bundling Microsoft products with its own managed services into a single SKU. Its ‘Essentials’ portfolio combines Microsoft 365 and Azure with governance, spend management, and backup solutions. Roughly 80% of CSP margins come from these bundled services and front-end spreads, while rebates make up the remainder, an entirely different margin profile to the old EA world.

Concurrently, SoftwareOne acting as a Tier 1 CSP, enables more than 100,000 smaller Managed Service Providers globally. These MSPs rely on SoftwareOne to deliver advanced capabilities like cloud migrations, managed security and licensing optimization, often on a white-label basis. This arrangement allows Microsoft to work with fewer, more capable Tier 1 partners, while ensuring end customers receive best-in-class service. The channel business now contributes roughly 15% of Microsoft-related revenue, grows at a double-digit rate and carries EBITDA margins near 70% -the most profitable segment within SoftwareOne today.

So, returning to Microsoft’s 2024 overhaul its incentive structure, it wanted to transition more end users away from EA and onto the CSP model. So it cut channel partner backend incentives on EA to just 50 basis points, while rewards for digital subscriptions sold through CSP channels were increased. At the same time, Microsoft tightened the criteria for becoming a Tier 1 CSP, signaling its intent to work with fewer but more capable strategic partners.

These changes are not merely administrative tweaks, they represent a clear strategic direction. Microsoft is steering customers toward evergreen digital contracts and deepening reliance on partners who can drive adoption in high-priority areas such as artificial intelligence and Copilot integration.

At the time of its 2019 IPO, on-premise EAs made up around 40% of Microsoft-related revenue. As Microsoft gradually phased out incentives for on-premise products, those economics shifted. Yet SoftwareOne’s total Microsoft revenues held steady even as gross billings nearly doubled, a reflection of how adeptly the company navigated changing incentive structures.

In this new landscape, success favours scale, technical sophistication and service depth. The bar for partnership has risen dramatically, and the benefits of meeting it have become more concentrated. The largest, most capable channel partners, those with the global reach, technical acumen and financial strength to align with Microsoft’s evolving model, are now positioned to capture the lion’s share of economic “rents” available in the ecosystem.

That’s precisely where SoftwareOne stands: among the select few global partners with the scale, credibility and adaptability to thrive as Microsoft’s ecosystem consolidates around its most strategic allies.

The SoftwareOne Eco-System & Strategic Advantage

Beyond Microsoft, SoftwareOne plays a vital role for enterprises managing sprawling IT estates that span hundreds of software vendors. As technology stacks become increasingly complex, the company’s position as an end-to-end licensing advisor becomes more indispensable.

Alongside Microsoft, SoftwareOne maintains substantial partnerships with Adobe, IBM, AWS, Google Cloud, Oracle, VMware, Red Hat, ServiceNow, SAP, HCL and others, which few competitors can match at similar scale. This one-stop-shop appeal reinforces its position with clients.

This non-Microsoft business accounts for about 35% of total licensing revenue, or CHF 270 million, and has grown at an annual rate of 12% over the past five years. Licensing margins here average around 6%, double that of Microsoft indirect EAs,reflecting the premium value SoftwareOne delivers in navigating multi-vendor environments.

Its solutions and services portfolio is where SoftwareOne’s durable competitive advantages shine. The business organizes its capabilities around three established “lead” categories: spend optimization, cloud access and workforce productivity; plus two fast-growing “expand” categories: cloud acceleration and data and AI adoption.

Spend Optimization is the strongest moat. SoftwareOne’s expertise in software asset management (SAM), IT asset management (ITAM) and cloud FinOps helps enterprises understand and control sprawling software costs. With IT spending averaging 8% of corporate revenue and cloud overruns commonplace, the need for visibility and control has never been greater. The merger with Crayon, owner of Anglepoint, another Gartner Magic Quadrant leader, positions SoftwareOne as the dominant force in SAM, employing over 1,200 specialists who deliver an estimated billion dollars in client savings annually. The impact creates a flywheel: cost savings free up budget, which is often reinvested in cloud projects that SoftwareOne then implements.

“To us, being recognized as a Leader again reflects our commitment to helping clients optimize their software investments and drive measurable business outcomes, which has been the backbone of our business model since the beginning”

Melissa Mulholland, Co-CEO, SoftwareOne

Cloud Access represents another core strength. Having guided thousands of organizations through cloud migrations across Azure, AWS, and Google Cloud, SoftwareOne holds a rare position as a trusted, multi-platform advisor.

Its Workforce Productivity practice complements this by modernizing how people work, deploying tools like Microsoft Copilot, embedding governance and security, and helping enterprises harness AI responsibly.

SoftwareOne’s achievement of Microsoft’s Copilot Specialization demonstrates advanced expertise in Microsoft 365 Copilot and AI-powered solutions, making it a trusted advisor for organizations adopting these cutting-edge technologies.

The “expand” categories are where the next leg of growth lies.

Cloud Acceleration focuses on modernizing legacy applications to fully exploit cloud-native architectures, an area with potential to exceed CHF 100 million in annual revenue.

Data and AI Services go further, with more than 650 experts delivering projects that span data unification, predictive analytics and generative AI adoption across industries. With deep relationships across all three hyperscalers, SoftwareOne is well placed to benefit as AI workloads scale globally.

Another area of strength is SAP services, a market exceeding $8 billion and growing quickly as enterprises prepare for SAP’s 2027 ECC support deadline. With over 500 SAP specialists and 600 completed projects, SoftwareOne is a proven leader in S/4HANA migrations and expects this practice alone to surpass CHF 100 million in revenue.

The company’s technology backbone is its Marketplace Platform, launched in 2016 as PyraCloud. It now connects 60,000 customers to over 2,000 software vendors, enabling discovery, procurement, compliance and spend optimization in a single interface. Billings through the platform grew 70% in 2024 to CHF 859 million, representing about 10% of SoftwareOne’s indirect volume. The platform not only digitizes an historically manual process but embeds SoftwareOne more deeply into client operations, creating sticky relationships and expanding margins through automation and self-service.

This infrastructure is also a strategic moat. Over a decade and CHF 100 million of investment have built an end-to-end digital procurement system unmatched by competitors. With Crayon’s Cloud-IQ platform now integrated - used by smaller MSPs to manage end clients from a unified dashboard - the combined offering is even stronger.

In short, SoftwareOne has evolved from a licensing intermediary into an integrated digital platform with unrivalled scale, deep vendor expertise, and a defensible technology advantage, an ecosystem that will be extraordinarily difficult for others to replicate.

Capital Allocation

Management has shown willingness to invest for growth: the series of acquisitions (including the bold Crayon takeover) indicates they will deploy capital when strategic opportunities arise. Thus far, acquisitions like Comparex (2019) and several cloud consultancies have been integrated without major issue, and Crayon – while a big bite – comes with a compelling strategic rationale.

The company maintains a meaningful dividend with a payout ratio ~40% of earnings. This is very European, but remember that this is a service business that has an engine that throws off cash. Retaining 60% of earnings seems to be sufficient to fuel growth both organically and through acquisition.

The disappointment comes from what seems to be a sacrifice of agility through the commitment to dividends. The recent collapse in the share price, which many would argue is overdone, presented a wonderful opportunity to engage in larger scale stock repurchases instead of dividends. Such a move would have undoubtedly been a more accretive use of capital, but opportunity cost seems not to have been evaluated by management. Unfortunately in Europe, dividends are considered sacrosanct and CEOs are not as adept at capital allocation as their North American peers.

If cost management is considered a form of capital allocation, albeit indirectly, one could argue that management was a bit slow to initiate the cost savings – only after Active Ownership Capital (an activist investor) became involved did they accelerate the cost cuts and upgrade the target from CHF 50M to 70M, before eventually saving 88M).

Risks & Mitigation

SoftwareOne faces a series of interconnected risks, notably the integration and execution risks following its large-scale merger with Crayon. While CHF 80–100 million in annual cost synergies have been identified, realizing them necessitates harmonizing systems, teams, and cultures within 18 months, with the risk of service disruptions or loss of key customers if mishandled. In mitigation, this acquisition is not its first rodeo. SoftwareOne overdelivered on expected synergies when it completed its huge Comparex acquisition in 2019. There is no reason to believe that it will not achieve great success again this time when integrating Crayon into its business.

While SoftwareOne experienced disruption in relation to some of its North American customer relationships, in emerging markets and APAC, SoftwareOne has been gaining share with strong double-digit growth - Asia-Pacific enjoyed 15.8% YoY revenue growth in 2024 thanks to booming cloud uptake in markets like India and Southeast Asia. The addition of Crayon’s strength in the Nordics and the additional expertise in AI and cloud services that Crayon is known for, makes the combined entity a formidable global competitor in the cloud services arena.

The company is heavily reliant on its key software vendors, particularly Microsoft, whose incentive program changes have already negatively affected SoftwareOne’s revenues and could continue to introduce margin and revenue volatility. A macroeconomic downturn or tightening IT spending cycles could further stagnate or contract growth, with reported results also sensitive to foreign currency swings (notably the strong CHF). The competitive environment remains intense, especially as hyperscalers promote direct cloud marketplaces, posing a structural threat to resellers. Post-acquisition leverage introduces new financial risks, particularly if execution falters and interest rates remain high. Additional risks stem from managerial turnover, the adoption of the new co-CEO structure post-merger, and evolving technological paradigms (e.g., automation, AI) which may require rapid adaptation of business offerings.

SoftwareOne’s revenue has a mix of high-quality and lower-quality components. On one hand, a considerable portion of revenue comes from recurring or repeat business: large enterprise license contracts often renew annually or every few years, and cloud subscriptions provide ongoing revenue streams. The addition of managed services (multi-year engagements) further improves visibility. On the other hand, the Marketplace segment (over half of revenue) can be volatile and transactional, with volume driven by clients’ procurement cycles and vendor incentive schemes.

The recent Microsoft incentive changes highlight that revenue is not fully in SoftwareOne’s control. The reliance on third-party product sales means relatively low margins and, while unlikely, it is always susceptible to disintermediation if the hyperscalers pursue some form of direct to market platform approach to sales. As software procurement becomes more automated and vendors push direct sales, the traditional reseller role could diminish. SoftwareOne’s answer is its Client Portal and value-added services, essentially moving up the value chain, evolving into more of a solutions provider - not just a reseller.

Some of SoftwareOne’s services (e.g. basic license resale) don’t have high barriers to entry – competitors can undercut or customers can internalize the function, so it must keep differentiating. That said, the scale and relationships it has built form a moat of sorts, and the integrated model (combining licensing and services) is not easily replicated by smaller firms.

The rise of AI and cloud actually plays to SoftwareOne’s strengths - the proliferation of SaaS, cloud and hybrid IT environments increases complexity, which sustains demand for a “software solutions aggregator” like SoftwareOne. Additionally, its services revenue (almost half the mix) is higher quality – it’s stickier, often project-based but increasingly with recurring support contracts, and tends to have client relationships that are harder to displace.

Moreover, the company’s push into cloud advisory, FinOps (cloud financial management), and software lifecycle management services indicates an effort to boost revenue quality.

Bear in mind that goodwill and intangibles will increase with the Crayon acquisition, so there is always a risk of impairment if performance disappoints, although it did not over-pay for Crayon

Is SoftwareOne a Good Investment?

Valuation and Investment Thesis

SoftwareOne’s scale and global reach are key differentiators. The merger with Crayon creates a combined company with CHF ~16 billion in annual customer billings managed (on behalf of clients) and operations in over 70 countries

On the subject of customer billings, when analyzing this company, it should be noted that the top line includes pass-through licensing costs, so not all revenue reported belongs to SoftwareOne. The company’s “gross profit” is a better gauge of its actual revenue quality.

Its scale provides bargaining power with major software vendors and the ability to serve multinational clients with consistent service delivery worldwide. According to Microsoft’s Chief Partner Officer, the combination makes SoftwareOne-Crayon “one of our largest partners, better positioned than ever to serve our mutual customers with broader reach, deeper expertise, and enhanced capabilities”

With an asset-light model and now greater scale, SoftwareOne’s financial health is robust. Prior to the Crayon deal, the company was effectively debt-free with net cash on the balance sheet and it consistently generated positive operating cash flow. With the acquisition, the company has taken on debt, but management has committed to keeping net debt/EBITDA below 2x and intends to refinance and pay down the bridge loan quickly (post-merger, they likely have access to credit lines and the cash generation of a larger entity.)

Even at 2x leverage, that is a comfortable level for a business with high recurring revenues and EBITDA margins ~20%+. Interest coverage should remain healthy (especially as a portion of the acquisition was financed with stock, limiting debt needs).

The company also benefits from negative working capital (after factoring) of around CHF -155M, which means it gets cash from customers faster than it pays suppliers – a structural cash flow advantage.

The transformative merger with Crayon creates one of the world’s largest software-and-cloud solutions platforms, full of promise for accelerated growth and substantial cost synergies. The strategic merger broadens the service portfolio and geographic reach, positioning the company to capture more growth opportunities in areas like AWS/cloud services, AI solutions, and mid-market customers (leveraging Crayon’s strengths). In essence, SoftwareOne is transitioning from a traditional reseller to a global, services-oriented, integrated solutions provider, supported by a strategic roadmap (Vision 2026) focused on reigniting growth, improving margins and maximizing long-term value. This is strategic and it ensures durability of earnings going forward.

More particularly, the secular drivers underlying SoftwareOne’s business – cloud adoption, software proliferation, data/AI investments – remain robust. The company’s target serviceable market is projected to grow about 17% CAGR through 2026, indicating plenty of headroom if SoftwareOne can execute. The company is quietly confident and has set ambitious internal targets (mid-teens organic growth by 2026) and is pursuing the strategic initiatives (hyperscaler partnerships, client portal, etc.) to get there.

SoftwareOne’s recent financial performance has been mixed. In FY 2024, net revenue grew only 2.9% (constant currency) to CHF 1,017M, falling short of earlier ambitions, with profitability squeezed by sales disruptions and cost inflation, adjusted EBITDA declined ~8% to CHF 223M (21.9% margin). The company finished 2024 with modest net profit (CHF 73M adjusted), and cash flow from operations dipped to CHF 37M, though it maintained a net cash position before the Crayon deal. In Q1 2025, revenue fell 5.7% YoY (reflecting tough comps and salesforce disruption), but EBITDA margin improved (19.8%) as cost reductions outpaced revenue losses.

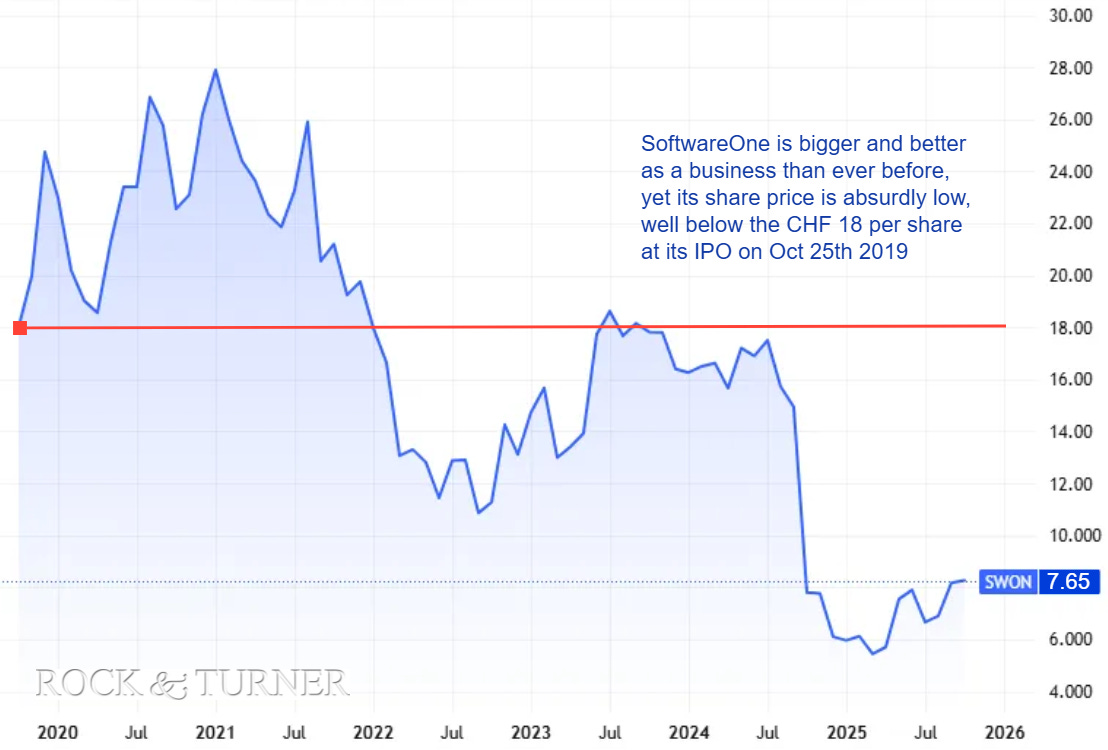

The turbulence of 2024 caused SoftwareOne’s share price to collapse, losing two-thirds of its market capitalization in just six months. The market’s reaction was brutal and, arguably, disconnected from reality. While the profit warning related to Microsoft’s incentive changes was certainly a setback, investors appeared to extrapolate near-term pain into long-term decline - an interpretation at odds with the company’s fundamentals, leadership reset and improving operational trajectory.

The most significant headwind came from Microsoft’s decision to restructure its backend incentives for Enterprise Agreements across all customer tiers. Level A, B and C rebates were reduced to match Level D1 at just fifty basis points. For SoftwareOne, that represented roughly a CHF 100 million headwind, partially offset by increased incentives under the Cloud Solution Provider (CSP) program and new pre- and post-sale service rewards. The net effect: mid-single-digit negative revenue contraction in 2025, followed by normalization.

Crucially, the underlying business remains solid. Microsoft-related gross billings continue to grow at a healthy high single-digit rate, supported by strong customer retention and forward visibility. There are no structural weakness in SoftwareOne’s Microsoft practice, only a temporary pricing adjustment. With rebate rates now standardized, management believed 2025 would mark the absolute trough in EA incentive compression. From here, revenue should more closely mirror billing growth. And even if Microsoft were to trim incentives further, the impact would be marginal given the already low base.

It’s also important to remember that most of SoftwareOne’s Microsoft revenue comes from indirect agreements, where it controls client pricing and invoices directly. In these contracts, backend rebates are just one component of total margin. The company can adjust front-end pricing and bundle more value-added services to offset lost incentives, a structural flexibility most smaller partners lack.

Taken together, the outlook is far more resilient than the market implies. Going forward, management expects mid-teens EBITDA growth driven by substantial cost savings and early synergy realization from the Crayon merger. In other words, while sentiment remains anchored in prior year’s turbulence, the fundamentals suggest an inflection point, one that forward-looking investors would do well to notice.

The turnaround is taking longer than anticipated, but that doesn’t mean it isn’t happening. On October 31, 2025, SoftwareOne announced a significant downward revision of its full-year revenue growth forecast from 7-9% to just 2-5%, citing underperformance in most regions except Asia-Pacific and German-speaking markets. This has impacted investor sentiment and the share price remains weak. To compound matters, we have recently experienced increased volatility in tech and software stocks, influenced by macroeconomic uncertainties, inflation concerns and interest rate sensitivities - all of which can exacerbate declines caused by a disappointing announcement.

For investors not willing or able to do any qualitative analysis on SoftwareOne, the stock doesn’t screen well, but looking at data in the rear view mirror is not an advisable way to drive. The road ahead looks straight and clear, providing SoftwareOne with all that it needs to accelerate forwards.

The current market cap sits at CHF 1.7 billion (CHF ~7.40/share), for a combined entity that has roughly CHF 1.6 billion in net annual revenue - another sign of under valuation.

The dividend yield stands at an attractive ~3.8%, with a stated policy to pay 30–50% of adjusted net profit and maintain a healthy capital return approach post-merger. Valuation is undemanding, reflecting recent setbacks but offering rerating potential as fundamentals improve.

The current valuation appears undemanding if SoftwareOne can execute its plan. A forward P/E ~12× and EV/Sales ~1× (on a combined basis) are below typical multiples for global IT services/cloud solution providers. When viewed against peers, SoftwareOne’s valuation looks absurdly low. Comparable channel and IT services firms trade at healthy double-digit EV/EBITDA multiples: Bytes Technology Group at 11.4x, Softcat at 15.5x, Softchoice at 11.9x, CDW at 12.2x. Even Crayon, which SoftwareOne itself acquired earlier this year, at around 11.5x. The simple average comes out to 12.5x.

Now consider what SoftwareOne’s numbers will look like by 2026. Post-merger, the company will be generating the combined revenue and EBITDA of both itself and Crayon, bolstered by synergy savings and a layer of organic growth. Consensus estimates place 2026 EBITDA at around CHF 370 million. Yet the market currently values the entire enterprise at only CHF 1.1 billion - pretty much the price that it paid for Crayon - implying an EV/EBITDA multiple of just 2.97x.

Even applying a modest peer multiple of 11.5x, which is very conservative given SoftwareOne’s scale, recurring revenue base and cash-generative model, that implies an enterprise value of roughly CHF 4.26 billion. That’s nearly four times the current level.

Let’s project three plausible 5-year scenarios (2025-2030) for SoftwareOne’s total return, based on fundamental drivers. The three scenarios are: Optimistic, Realistic and Pessimistic- each being grounded in the company’s execution of its strategy, the integration of Crayon, and broader market conditions.

Optimistic Scenario:

SoftwareOne successfully transforms and achieves or exceeds its Vision 2026 goals. The integration of Crayon is smooth, unlocking the full CHF ~100M cost synergies within 18 months.

The combined company realizes revenue synergies by cross-selling to each other’s customer base and leveraging its enhanced capabilities – for example, Crayon’s channel platform and SoftwareOne’s services portfolio drive expanded customer access across all segments. As a result, organic revenue growth accelerates to high-single or low-double-digits annually from 2026 onward.

Robust market demand (the cloud/software market grows ~ mid-teens % per year, and SoftwareOne gains share thanks to its broadened offerings). By 2030, assume the company’s revenue has grown at ~9–10% CAGR from the combined 2025 base (CHF ~1.6B), reaching roughly CHF 2.5–2.8 billion in annual sales. Growth is driven by cloud services, data & AI projects, and expansion in high-growth regions, while the traditional licensing business remains healthy.

Crucially, in this optimistic case SoftwareOne also achieves margin expansion. With cost synergies realized, adjusted EBITDA margins improve from ~22% in 2024 to the high-20s by 2026 (approaching the 27–28% target) and continue to inch upward thereafter (assume ~30% EBITDA margin by 2030 in this scenario). This could come from economies of scale, more higher-margin services in the mix, and continued operational excellence. The company maintains disciplined costs even as it grows.

On the capital allocation side, assume the dividend grows modestly with earnings (payout ratio ~40%). Also, by 2030 the debt taken for the acquisition is largely paid down (strong cash flows used to deleverage), bringing net debt/EBITDA back under 1×, which could potentially allow share buybacks or additional bolt-on acquisitions (not explicitly modeled, but any accretive M&A would add upside).

If SoftwareOne reaches ~CHF 2.6B revenue with 30% EBITDA margin, that’s ~CHF 780M EBITDA. Assuming a valuation multiple of ~9× EV/EBITDA (a reasonable multiple for a market leader with strong growth and moderate leverage), the enterprise value would be about CHF 7.0 billion. Subtracting negligible net debt (assumed mostly paid off by then), equity value is ~CHF 7.0B. With ~230 million shares (assuming no major change in share count), this yields a share price of roughly CHF 30 in 2030. This is more than 4× the current price. Even if we apply a more conservative multiple (say 8× EV/EBITDA or ~15× P/E), we’d still get a share price on the order of mid-20s CHF. Let’s be conservative and say CHF 25 as a rounded figure, which implies a very robust outcome (approximately 3.5x today’s share price, or ~27% annual compound growth plus dividends).

Pessimistic Scenario:

A combination of internal and external factors leads to underwhelming outcomes. The Crayon integration might encounter difficulties – perhaps cost synergies take longer or only, say, 50% of the targeted savings are realized within 5 years (the rest eaten up by integration costs or inefficiencies). Additionally, the merged company might face unexpected revenue attrition: for example, during integration some key customers or sales talent are lost, or execution issues persist in major markets (e.g. North America never fully recovers its momentum). Meanwhile, the macro environment could be tepid – assume global IT spend grows slowly, or even a mild recession hits, causing SoftwareOne’s revenue to stagnate around the current level. In this scenario, we might see flat to very low growth – revenue perhaps grows ~1-2% annually or oscillates with little trend. By 2030, revenues could be ~CHF 1.7B (essentially the combined 2025 level plus a bit).

Even with poor top-line performance, the company would still likely achieve some cost savings; thus, EBITDA margin might hold around 22–24% (basically similar to 2024 levels, as cost cuts offset lack of scale benefits). Let’s assume by 2030 an EBITDA of ~CHF 380–400M (margin ~23%). However, with growth disappointment, the market may view the company as ex-growth and assign a low multiple.

The stock could tread water or worse. Using a low multiple 6× EV/EBITDA (appropriate for a no-growth, possibly shrinking business), and ~CHF 390M EBITDA, gives EV ~CHF 2.34B. If net debt is still ~CHF 300M (could even rise if cash flows disappoint and dividends are still paid), equity value ~CHF 2.04B, spread over ~230M shares is about CHF 8.9 per share. Another approach: if net profit in this scenario remains around CHF ~80–100M (roughly where it was in 2023–24 adjusted), EPS maybe ~CHF 0.40, and a low P/E of 10× would yield a CHF 4.0 stock. Let’s take a midpoint and say the stock trades around CHF 6.5 range in five years. Note that even in this case, long-term shareholders might eke out a roughly breakeven total return if dividends (3-4% yield) are counted – but capital appreciation would be negative.

Realistic (middle-ground) Scenario:

SoftwareOne executes its integration and strategy reasonably well, but not perfectly. The full cost synergies from Crayon are realized on plan (CHF ~80M by 2026), providing a one-time boost to margins.

However, revenue growth is more moderate – perhaps ~5% CAGR over the next 5 years. This assumes the company restores steady growth but not quite the “mid-teens” ambition; some regions or segments continue to face headwinds (e.g. competition in Europe keeps pricing tight, or some Microsoft licensing volumes stagnate as more customers shift to direct cloud subscriptions). Still, 5% organic growth would be above recent performance and reflects successful elements of the strategy (for instance, services and emerging markets offsetting flat traditional sales). By 2030, revenues in this case reach around CHF 2.0–2.1 billion.The adjusted EBITDA margin improves to roughly 26–27% (near the low end of Vision 2026 target, but not significantly beyond). Synergies and prior cost cuts prop up margin, but ongoing investments in new offerings and some competitive pressure keep margins from expanding much further. Net-net, EBITDA might be ~CHF 550M by 2030 (on ~CHF 2.05B revenue at ~26.5% margin). The company maintains its dividend policy and cumulative dividends add to total return (we assume ~CHF 0.40 annual dividend by later years). Leverage is managed to <1.5× EBITDA; the company carries some debt but comfortably within its capacity, ensuring no distress.

In this middling scenario, SoftwareOne in 5 years is a stable, mid-growth company with solid (but not extraordinary) margins. Such a profile might warrant a valuation around 8× EV/EBITDA or roughly 12× P/E, – essentially in line with market averages for a stable IT services firm. Using 2030 EBITDA ~CHF 550M, 8× multiple yields EV ~CHF 4.4B. Subtracting, say, ~CHF 200M net debt (if some debt remains) results in an equity value ~CHF 4.2B, or ~CHF 18 per share. That might be on the higher side; to be conservative we could also derive from earnings: if net profit in 2030 is around CHF 200M (assuming ~36% EBITDA-to-net conversion, due to taxes, etc.), EPS would be ~CHF 0.87 (with 230M shares). A 14× P/E on that would give ~CHF 12, whereas a 18× P/E would give ~CHF 15. Blending these approaches, the realistic case price target would be CHF 15 in 5 years. This implies roughly double the current price (15% CAGR in stock price) augmented with the receipt of dividends.

With the stock already pricing in a worst-case scenario, downside appears limited while upside potential is substantial. It’s a classic asymmetric setup, one where the downside risk appears limited (the business is unlikely to structurally implode given its entrenched client base and cash generation), but the upside reward could be transformative. In short, heads you win big; tails, you don’t lose much at all.

The investment opportunity exists, primarily because, since its IPO in 2019, SoftwareOne’s track record of delivering shareholder value has been patchy. The stock, as of mid-2025, trades significantly below its IPO price (which was around CHF 18) and well below highs after the exceptional 2024 share price collapse. This has hurt the credibility of the company in the eyes of the market, but as I always like to say, the same company with different management is not the same company. Everything has changed in the last 12 months and SoftwareOne today is not the SoftwareOne of a year ago.

Additionally, be reminded that Bain Capital was interested in taking SoftwareOne private at CHF 20.50 per share earlier this year. Bain were not alone. Apax Partners and CVC2 had also expressed an interest back in 2024.

The fact that private equity has expressed an interest in this business suggests that eagle-eyed professional investors saw value that public markets were not recognizing. That was prior to the restructuring and before the Crayon merger which enhanced its value further. Today the shares are available to you and me at CHF 7.50 - essentially we can buy SoftwareOne for 33% of the price that private equity were willing to pay, and, if that discount is not enough, we get Crayon thrown in for free - food for thought.

If the public markets undervalue the stock persistently, there is always the possibility of renewed takeover interest.

Does SoftwareOne present a compelling turnaround and value-unlocking story? Only you can decide - this is not investment advice!

The four EA levels with specific user counts (Level A: 500-2,399, Level B: 2,400-5,999, Level C: 6,000-14,999, Level D: 15,000+)

Q3 2025 Results

Raphael Erb and Melissa Mulholland, Co-CEOs of SoftwareOne said, “The third quarter marked our first as a combined company – an important milestone in our journey to create a global leader in software and cloud services. We are encouraged to see early signs of growth recovery, as well as improved profitability driven by strict cost control and disciplined execution. Cost synergy realization is progressing well, and as we move into the fourth quarter, we are increasing our focus on our strategic sales plays and joint go-to-market approach to capture additional revenue opportunities. With our strong position across the cloud and AI value chain, we are well placed to harness the next wave of demand and deliver sustainable, profitable growth.“

↪ Revenue increased 46.0% year-on-year on a reported basis in Q3 2025 and 8.6% year‑to‑date, reflecting the Crayon acquisition

↪ Reported EBITDA rose by CHF 29.5 million to CHF 42.0 million in the quarter and by CHF 32.4 million to CHF 127.0 million year‑to‑date

↪ Integration progressing as planned with CHF 21 million of run-rate cost synergies achieved by the beginning of November 2025 – well on track to realize 30% of total run-rate cost synergies by end of 2025 and deliver CHF 80-100 million run-rate cost synergies by end‑2026

↪ On a combined like-for-like basis (as if the acquisition of Crayon had been completed on 1 January 2024) Q3 2025 revenue growth ended at 0.6% at constant currency with an adjusted EBITDA margin of 19.0%, up 2.9 percentage points compared to the prior year

↪ FY 2025 outlook unchanged: on a combined like-for-like basis, revenue growth expected to be flat in constant currency compared to 2024, with an adjusted EBITDA margin expected to be above 20%

Brilliant. Thank you for finding these gems in such an overvalued market!!!