Somero Enterprises | Deep Value

Market Leader in Concrete Levelling Technology

Name: Somero Enterprises Plc Ticker: SOM Exchange: London

Founded: 1985

Industry: Industrials

Implied Market Cap: £160m GBP

Theme: Deep Value Assessment: Buy The Dip Author’s Strategy: Long

Disclaimer:

Views, information and opinions expressed in this analysis are those of the author. They should neither be construed as investment advice nor as a recommendation to buy or sell any particular security. Security specific information should not be relied upon as the basis for your own investment decisions. You must do your own research, seek independent advice and reach your own conclusions.

The author may have a position in securities named in this article and may change those position at any time

The Company

Somero is a global leader in the development and manufacture of laser-guided concrete leveling equipment.

When building a residential property, which is relatively small, floor leveling requirements are not so strict. A few millimeters out and it doesn’t compromise the integrity of the building. But if you are building a huge structure, a shopping-mall, an airport or a factory, then leveling is super important and there are strict regulations to comply with. This is where Somero equipment excels. Lasers ensure concrete is perfectly level. Not only do they do the job better than before, but they improve making concrete placement cheaper and faster.

Somero equipment has been used in construction projects around the world for a wide-array of the world’s largest organizations including Costco, Wal-Mart, Home Depot, B&Q, Carrefour, IKEA, Mercedes-Benz, Coca-Cola, FedEx, the United States Postal Service, Lowe’s, Toys ‘R’ Us, Tesla, Cadbury and ProLogis.

The company's products are now used by customers in over 90 countries with operations in North America, Europe, and Asia.

Somero was founded in 1985 and is headquartered in Fort Myers, Florida. In the years since its founding, Somero has continued to innovate and develop new products and technologies that have helped to improve the efficiency and productivity of concrete leveling. The company employs over 300 people, and it has a global network of sales and service representatives.

Key Investment Data

Founded 1985

Currently valued at approx 4.5x EBITDA

Net cash position (No long term debt)

On a debt free/cash free basis, currently valued at 3.24x EBITDA

Implied valuation is only 1.57x revenue (1.33x enterprise value) on profit margins of circa 22%

Hugely cash generative

It generates so much cash that it pays out strong dividends

Leader in a niche market with a great deal of growth ahead of it (currently 73% of revenue in North America, but huge international expansion underway)

Won lots of awards for being one of the best places to work, being an ethical company and for sustainable excellence

Recently seen revenues hit an all time high. Top line has been compounding at almost 10% CAGR for over a decade (almost all organic), 9.8% for the last 5 years.

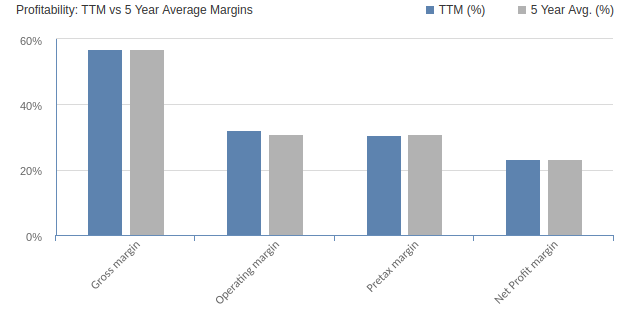

High gross margins consistently >55%

Earnings margins 20%-22%

RoE and ROIC both circa 40%

90% cash conversion rate

Most growth investment is expensed rather than capitalized, so no smoke and mirrors on D&A

Balance sheet cash > PPE carrying value, so a capital light operation

Sells machinery plus offers a full maintenance, support and training service, so recurring revenues

Return on net tangible assets is almost 40%

Long term CEO, appointed 2005, been with Somero since 1997

A great deal of value to be unlocked.

The stock has traded 67% higher than its current stock price and, based on these fundamentals, I believe it is worth more than that today. This really is a buy the dip opportunity and a positive asymmetric skew.

Ownership Structure

Somero is a publicly traded company on the London Stock Exchange.

The business is owned by a diversified group of shareholders:

Insiders have a relatively small ownership. The CEO, Jack Cooney, circled above holds just over 1% worth over $2m USD, so he certainly has skin in the game.

The two founders of the company are currently aged 82 and 62 respectively and Cooney (77), who joined the the company in 1997, has served as CEO since 2005.

Ownership of the remainder is split between retail investors and institutions, although many of these institutions are asset managers buying on behalf of retail investors. The company is currently too small for big institutional funds portfolio, but as it grows its market capitalization, it will soon breach the threshold at which the bigger fish starts to take notice. At that point it catches the wave of money which ought to propel it further.

Recent Accomplishments

In 2019, the company introduced the Somero SR700, the world's first self-propelled laser screed. The SR700 is a major technological advancement that has further improved the efficiency and productivity of concrete leveling.

In 2020, the company reported record sales and earnings. The company's strong performance was driven by strong demand for its products and services, as well as the continued growth of the global concrete industry.

In 2021, the company was named one of the "Best Places to Work in America" by Fortune magazine. The company's strong employee culture and commitment to innovation were cited as key factors in its selection. It was named one of the "World's Most Ethical Companies" by the Ethisphere Institute. Somero was also awarded the "Sustainable Excellence Award" by the Concrete Institute of Australia.

In 2022, the company reported record sales and earnings. The company also expanded its global footprint, opening new offices in China and India which bodes well for the future given the size and population of both countries together with the rate at which they are investing in infrastructure projects.

In 2023, Somero has continued to grow its business. The company has introduced new products, and it has expanded its sales and service network. Somero is well-positioned for continued growth in the years to come.

Customer First Philosophy

Laser Screeds: Somero's laser screeds are the most advanced concrete leveling equipment on the market. They use a laser guidance system to ensure that concrete is leveled to a precise degree. This makes it possible for contractors to place concrete faster and with fewer errors. Its machines are used in a wide variety of projects, including warehouses, factories, parking garages, and airport runways.

Concrete Training: Somero offers a variety of concrete training programs to help contractors learn how to use its products effectively. These programs include flying Somero people around the world to the customer’s location for hands-on training in addition to classroom instruction, and online courses.

Concrete Support: Somero provides 24/7 support to its customers. This support includes technical assistance, parts and service.

Financials

Top line revenue is trending upwards and so too are economic earnings. Top line has been growing at >9% CAGR for over a decade.

Margins are incredibly stable, the sign of a market leader in a niche market with limited competition.

Returns are very impressive. >40% RoE and RoIC

A fortress of a balance sheet with zero long term debt and a net cash position.

The company generates so much cash that it had a 93% dividend payout ratio last year amounting to a 12% dividend yield. It’s dividend has averaged 5% over the past 12 years and 7% over the last 5 years.

Looking forward, top line growth looks like continuing as the global expansion for Somero continues. At the moment 76% of its business is North America and so there is a huge amount of global TAM ahead. It is now operating in both India and China, both being very densely populated and rapid development in both countries means more concrete laying.

In 2020, the global cement production was 4.1 billion tonnes. China is the world's largest producer of cement, followed by India, the United States, and Japan.

It is worthy of note that investment in its international expansion, which will pay big dividends in the medium and long term, is what has impacted this year’s profits. Although revenues are up, net income and cash flow from operations are naturally down. As explained earlier, most of Somero cost base is OPEX rather than CAPEX and so spending has a more pronounced impact on the bottom line this year, but with relatively little capitalized spending to depreciate in subsequent years.

Investing for long-term growth:

The US$ 9.5m expansion project for the Houghton, Michigan, Operations and Support Offices was completed in 2022 and expected to be fully operational in early H1 2023

The Company continued to add employees in 2022 with a focus on global sales and customer support, and domestic operational roles

The knee jerk reaction of Wall Street and lazy retail investors is that EPS is down so we sell, hence the dip in price. If they took the time to look under the hood, they would see that the business is stronger than ever and that the future looks very bright:

The focus on Europe via investments in people and local stocking levels drove a 23% annual sales increase to US$ 14.9m (2021: US$ 12.1m) marking an all-time high

The Australian direct sales and support team established in late 2020 and a broader representation of the Company’s product offering drove a 38% annual sales increase to US$ 8.4m (2021: US$ 6.1m)

The SkyScreed® 36, S-PS50, SkyStrip® and Somero Broom+CureTM, all launched since 2019 to target new market segments, combined to contribute US$ 4.2m to 2022 revenues (2021: US$ 3.2m)

The customer-led product development process made substantial progress in 2022 driven by a high volume of job site visits with customers and innovation council events

The Buying Opportunity

On 20th June, Somero provided a trading update. It reported that:

Tighter macro economic conditions (interest rates and restricted bank lending) have impacted the construction industry. This has “led to an increase in delayed starts to non-residential construction projects.” Importantly, they speak about delays and not cancellations of these projects. They go on to say “While US customers have not reported project cancellations, certain customers have indicated these project delays have impacted the timing of their equipment purchase decisions.” This implies that the sales will happen but are simply being pushed back.

“the S-22EZ (Somero machine), re-launched in early 2023, is not scheduled to reach full production until the end of H1 2023", and its limited availability has delayed sales to customers with a preference for it.” So once again, customers are pushing back orders until the S-22EZ is available, rather than buying an alternative machine. Again, the implication is that we are likely to see a big uplift in revenues achieved in H2 2023 and beyond.

There is currently a global shortage of concrete, including across the US. The winter construction season last year was milder so there was an unprecedented demand for cement, so cement producers were not able to build their inventory as they normally do during the winter months. Concrete prices are soaring both due to the shortages, but also due to energy price inflation (concrete production is an energy-intensive commodity) augmented with carbon reduction compliance costs. The war in Ukraine coming so soon after the supply shock of the Covid19 pandemic has created turbulence in the industry. All of this has also resulted in delays in construction projects.

As the result of these ‘short-term’ factors, the Company expects FY 2023 revenue and EBITDA to be approximately 10% below FY22.

So this caused a dip in the price. A knee-jerk reaction, creating a wonderful buying opportunity.

The medium term still looks great:

Lowered expectations for H1 2023 and FY 2023 revenue have been driven primarily by the US market. Somero continues to anticipate strong contributions to 2023 revenue from Europe, Australia, and the Rest of World territories, with Europe and Australia each expected to report H1 2023 revenue that meets or exceeds the comparable H1 2022 total.

Somero's operating model enables it to adjust quickly to changing circumstances. Due to the anticipated 10% reduction in 2023 sales compared to previous expectations, the Company has reduced its operational workforce by 10%. The workforce reduction combined with strict cost controls for the remainder of 2023 partly offset the profitability impact of the revised 2023 revenue expectations.

The impact of these efforts along with maintaining accounts receivable at low levels are anticipated to have a positive impact on year-end cash, anticipated to be US$ 32.0m (compared to the previous market consensus estimate of US$31.0m)

The Company anticipates an improvement in H2 2023 revenues over H1 2023 driven primarily by increased availability of the S-22EZ during the second half of the year.

If these issues are merely delays and the revenue will simply flow at a later date, then the investment thesis remains intact. Somero is still the market leader in this niche and, unless you believe that construction is dead, this is a wonderful business to invest in.

Steve Jobs once said, "Don't focus on what's going to change in the next 10 years. Instead, focus on what's not going to change. Because that's where your opportunity lies." So many people invest in the next big thing, but if you invest in a rapidly evolving industry, there will be high competition, there can be no certainty about durability of earnings because products become outdated quickly and capital intensity is high due to perpetual R&D investment. The better investments are in those dull industries that won’t change. Construction and concrete is one of them.

Analysis

Those readers familiar with my analysis will know that I dislike DCF models and that I make my own adjustments to reported numbers in order to discover the true economic earnings of the business (a variation of Buffett’s Owner Earnings concept - see his 1986 shareholder letter).

My adjusted numbers are as follows and are smoothed using moving averages over a longer time frame in order to remove any short term noise.

There are two tables below.

Looking back over the past 5 years (first table), revenue has grown at 9.8% CAGR, the share count is relatively unchanged, the economic earnings margin has expanded from 18.95% to 22.18%, average dividend has been 7%. All really good, except for the earnings multiple which has inexplicably collapsed. The company is currently trading at 7.06x economic earnings whereas it usually trades in the mid-teens. Therein lies a good reason to invest. Said differently, despite the stellar performance described above, total shareholder return over the past year has only been 37.3% (6.55% CAGR) which is bad news for yesterday’s investors. The share price was £3.07 GBP in 2017 and today is only £3.00 GBP despite the strong organic growth and improved margins. The shares were trading at over £5.80 little over a year ago before the Russian invasion of Ukraine but have been pulled down as the tide went out. (Be reminded that the stock is listed in London so the share price is in pounds whereas the accounting currency is US Dollars - so make the necessary adjustments when running your own analysis).

The second table is my assessment of the next five years. There is no good reason to believe that top line growth can’t continue at c.9% (conservatively less than the 9.8% of the past 5 years), particularly with the international expansion. I have assumed that the reduction in share count is at the same rate as before. Rather than any further margin expansion, I am assuming a slight contraction due to the macro-economic turbulence, but with zero debt there is no impact from higher funding costs and inflationary pressures on input costs can almost certainly be passed through, so this is a super conservative assumption. I have assumed that the dividend continues at levels similar to before, 7%. However, the big catalyst is the reversal of the multiple contraction. With earnings margins at over 20%, this stock could justify trading at over 2.2x sales, but currently only trades at just over 1.5x sales, so that provides the big kicker. On the basis of these projections, over the next five years shareholders could be looking at a total return of 194% (24% CAGR) on this stock. By the end of full year 2027, the share price could feasibly be £6.59 GBP which is not far off where they were a year ago.

My conservative assumptions provide a margin of safety. But even if the company under performs my assumptions, in the unlikely event that returns are only half of what I anticipate, you still have 12% compounded growth. I don’t see a scenario in which you would lose money and so the asymmetric skew is very favourable.

One Issue To Flag

My only complaint is that the company only engages in a small amount of share repurchases, largely to offset dilution as the result of RSUs issued to employees as a part of their remuneration plan. Stock based compensation seems entirely unnecessary for a cash generating machine, but it is relatively modest at 0.9% of top line and 3.95% of the bottom line so I am not overly concerned. However, with the stock price being so heavily discounted, the opportunity-cost of paying out huge dividends and not repurchasing more equity is huge.

The company paid out $14.2m in dividends and only authorized a share buyback program of aggregate value up to $2m ‘to offset dilution from on-going equity award programs’, so no reduction in share count and so no shareholder benefit.

I have challenged the company on this subject, but I can’t get past the investor relations people who, frankly, are PR people and not financial people. Their standard line is that this is the way that the company has always distributed capital and it has no intention to change. This is really disappointing and points to a lack of competence at the top when it comes to understanding which capital allocation levers to pull. I guess that to a hammer everything is a nail, and to a concrete man everything is set in stone!

It is worth pointing out that Jack Cooney, the CEO, joined the the company in 1997 and became CEO in 2005. He is aged 77. He has his way of doing things and it is unlikely to change. As the old saying goes, you can’t teach an old dog new tricks. The non-executive Chairman, Lawrence Horsch, joined Somero back in 2009 and is currently aged 89, so the same applies to him. On the flip side, one has to imagine that Cooney will hand the reigns over to a successor in the not too distant future and hopefully that person will have a better understanding of which capital allocation levers to pull and when to pull them.

Conclusion

This is a niche company operating in a “boring” industry. That’s what makes it great. A funky industry such as tech attracts too much attention and too many competitors. It reminds me of a comment made by Yogi Berra who said of a famous Miami Beach restaurant, “It’s so popular, nobody goes there anymore!” What was once a great restaurant is now having to compete with many great restaurants in the Miami Beach area. That doesn’t bode well for durable earnings.

By contrast, a niche business in a boring industry attracts little or no attention. The industry itself doesn’t need to be growing at a rapid rate, the company simply grows its customer base and churns out money year after year. That is durable earnings. That is the holy grail for investors.

Did you know that after water, cement is the most consumed commodity on earth? And as population grows, so too does consumption. If you are providing market leading equipment to lay concrete, you are pretty well placed as a business.

Did you know that in the gold rush of 1849, those that did the best were the suppliers of the picks and shovels. Sometimes it is better to be a second order beneficiary rather than focusing on the primary commodity itself. Somero is selling the best picks and shovels in the cement business.

Good article, this is a businesses I have been researching over the last few weeks. One thing I can't work out is why are they listed in the UK rather than the USA where they are based and have most of their business at present. Even if they moved now they are large enough for a proper listing and would likely have a much higher valuation?

Wednesday, 6 September 2023, 3:00pm UK Time

An interim results webinar will be given by Chief Executive Officer Jack Cooney, President John Yuncza and Chief Financial Officer Vincenzo LiCausi.

https://www.research-tree.com/events/piworld-co-uk/somero-som-interim-results-webinar-br-/1621