Three Stories Every Investor Should Know

The only thing we learn from history, is that most people don't learn from history!

, Png Download")

There are three stories that every investor should know. They lay the foundations for the way we need to think and provide mental models to help us navigate the markets.

I recently told these stories while lecturing an MBA class at the University of Buckingham in England. They were so well received that I decided to document them here.

Enjoy!

1. The Chevalier de Méré

In the bustling streets of Paris in 1650, a clever man named the Chevalier de Méré roamed aristocratic clubs with a mind that worked like clockwork. The Chevalier had made a discovery - he could win at dice, not through luck, but by skewing the odds in his favour. He knew the probability of rolling a six on a die was one in six, or about 16.7%. But what intrigued him was that after four rolls, the odds of seeing a six climbed to just over 50%. Armed with this knowledge, the Chevalier devised a plan to quietly extract wealth from the noblemen who frequented the salons of Paris.

He would bet small amounts, never enough to arouse suspicion, and challenge the wealthy aristocrats to a seemingly even game. The rules were simple: if he rolled a six within four rolls, he won a gold coin; if he failed, he would pay his opponent. What his opponents didn’t realize was that the odds were subtly tilted in the Chevalier’s favour. To the untrained eye, the game seemed fair, but the Chevalier knew that over the long haul, he was almost guaranteed to win more than he lost. His secret was to play small, play often, and keep the odds skewed ever so slightly in his favour - a tactic not unlike the ones casinos still use today.

“Investing is a long-term game. It takes time to build wealth. Don't expect to get rich quick. Be patient and disciplined, and you will eventually be rewarded."

Howard Marks

For a while, the Chevalier’s strategy worked flawlessly. He accumulated wealth as the aristocrats lost small amounts in what appeared to be an innocent game of chance. But like many who find success, the Chevalier’s confidence grew, and soon, he sought to refine his system. He invented a new game, betting that a double-six would appear in 24 rolls of a pair of dice. However, his calculations this time were flawed. The probability of rolling double-six in 24 rolls was just under 50%, and the edge that had once made him invincible slipped away. His losses mounted, and he found himself on the brink of financial ruin.

In desperation, he reached out to his brilliant friend Blaise Pascal, the renowned mathematician, for help. Pascal, intrigued by the problem, collaborated with Pierre de Fermat, another mathematical giant. Together, they worked out the flaw in Chevalier’s calculations. Their correspondence in 1654 became a foundational moment in the development of probability theory.

This was arguably the pivotal moment in history that marked the beginnings of the modern day casino.

Pascal’s involvement with probability theory didn’t stop with the Chevalier’s dice game. His famous philosophical dilemma, now known as Pascal’s Wager, posed a binary question: ‘Does God exists or not?’ Pascal reasoned that if you believed in God’s existence and were wrong, the downside was minimal. However, if you bet against God's existence and were wrong, the consequences could be eternal damnation. As such, Pascal underwent a profound personal transformation, turning away from mathematics and embracing a life of religious devotion locked away in a monastery for the remainder of his days.

“Prioritize the downside of every investment. With limited downside, the upside will take care of itself.”

Howard Marks

For investors, Pascal’s Wager holds a powerful lesson. Every investment decision is a binary choice: should you invest or not? The way to tackle this problem is to consider the downside if you’re wrong. Much like Pascal’s spiritual deliberation, a wise investor considers the risk of loss as much as the potential for gain.

“A bird in the hand is worth two in the bush”, is one of the oldest and best-known proverbs in the English language. It dates back to at least the 15th century. The proverb warns against taking unnecessary risks: better to hold onto what you have - a bird - than to gamble on the promise of two elusive birds in the bush, only to end up with nothing.

But is this proverb really the whole story? It doesn't factor in the value of time. If you could trade that one bird today for two tomorrow, that sounds like a pretty good deal. But it could take years to actually snag those two birds from the bush. Is the risk still worth taking? The answer lies in weighing the odds - calculating risk, just as the Chevalier de Méré did when pondering probability centuries ago.

Then there are cases where someone will over pay for your bird, in the belief that someone else will pay them a higher price tomorrow. This they call the "greater fool theory," which is not investing at all - it involves no shrewd calculations, no weighing of risks, just the giddy hope that someone else will come along with even wilder dreams and greedier aspirations tomorrow.

This kind of speculative madness has popped up throughout history: from the craze over tulip bulbs in 1600s Amsterdam (yes, tulips - flower power gone financial), to the infamous South Sea bubble of the 1700s, all the way to the dot-com frenzy and cryptocurrency hype in our own times. The playbook is always the same: prices skyrocket far beyond any reasonable assessment of intrinsic value, investors trip over themselves to get in on the action, the media fans the flames, and before you know it, everyone is convinced that they are going to be rich. Then, predictably, it all unravels leaving everyone to wonder how they ever believed in bushes full of birds in the first place!

On the subject of calculated risk-taking, the next character in our story is found across the English Channel in 18th-century London. His name is John Henry Martindale and he devised what would become known as the Martingale strategy. The idea was straightforward: place a bet on an even-money outcome, and if you lose, double your stake on the next round. Theoretically, your first win would recover all previous losses and leave you with a small profit equal to your initial stake. But there was a catch - if a losing streak lasted too long, the capital required to keep doubling your bets would skyrocket. The Martingale strategy, seductive in its simplicity, was a financial trap for those who underestimated the risks of exponential loss.

“How much a company earns on the capital invested in it is the best measure of how it is doing. From both financial and philosophical points of view, that's what counts."

Robert Pritzker

The lesson for modern traders is clear: achieving a gain is not enough. The capital, time, and risk involved in securing that gain must also be weighed. It is all about return on invested capital and having access to the requisite capital in the first instance.

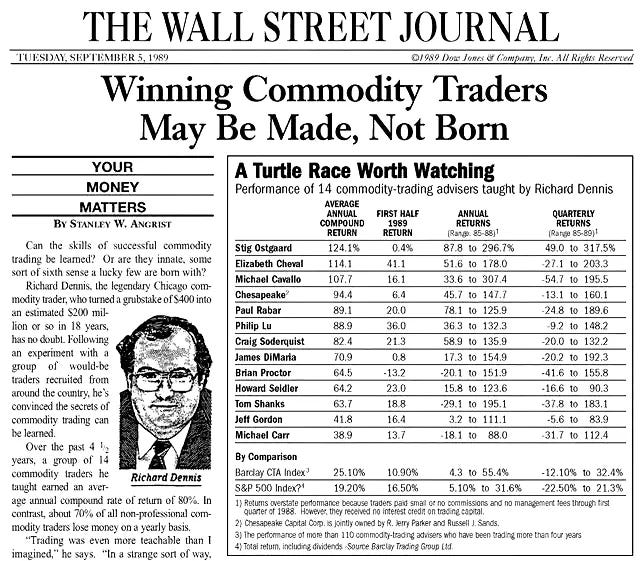

2. The Turtles

Fast-forward to 1983, Chicago. Two legendary traders, Richard Dennis and Bill Eckhardt, found themselves in bar having a heated debate over the nature of trading success. Could great traders be made, or were they born with a unique set of personality traits?

This was the classic nature or nurture debate in the context of investing. Dennis believed anyone could be taught to trade successfully, while Eckhardt argued that trading prowess was innate. The two friends placed a $1 million wager, and to settle the debate, Dennis devised an experiment that would make financial history, giving rise to the legendary Turtle Traders.

Dennis advertised in major newspapers:

Despite this being a wonderful opportunity, very few applied. However, thirteen individuals with no prior trading experience were selected.

Over the next several months, Dennis taught them his method, drilled them in the rules of trading, and gave each of them a large sum of money to manage.

The result? The Turtle Traders earned over $175 million in five years, proving that trading success was not about intuition or natural ability, but about discipline, risk management, and following a system.

Richard Dennis won the bet, but his $1m winnings paled into insignificance relative to the money that he made from trading.

“Trading was more teachable than I ever imagined. Even though I was the only one who thought it was teachable . . . it was teach able beyond my wildest imagination.”

Richard Dennis

At the heart of the Turtle Traders’ success were six essential rules. These rules, if followed religiously, could skew the odds in any trader’s favour:

1. Markets – What to Buy: The first rule of trading was to select markets wisely. Dennis taught the Turtles to focus on specific markets - commodities, futures, or stocks - but to avoid being “a jack of all trades.” Specializing allowed them to understand the nuances of their chosen market and to recognize valuable opportunities. By becoming experts in their market, they skewed the odds of making profitable trades in their favour.

2. Position Sizing – How Much to Buy: The second rule was all about managing risk. No matter how confident a Turtle was about a particular trade, they were taught never to risk more than a small percentage of their total capital on any one trade. Dennis’s rule was simple: never risk more than 2% of your portfolio on a single position. This ensured that even in a losing streak, their capital wouldn’t be wiped out - a crucial lesson that echoes the Chevalier’s strategy of placing many small bets.

3. Entries – When to Buy: Timing was everything. The Turtles learned to enter trades based on a set of technical indicators, mainly using price breakouts. If a commodity or stock reached a certain threshold, it triggered a buy signal. This rule minimized the emotional decision-making that plagues many amateur traders and ensured that they only entered trades when the odds were in their favour.

4. Managing What You’ve Bought: Once in a trade, the Turtles had to know how to manage it. Dennis taught them the importance of letting winning trades run, while cutting losses quickly. This was a fundamental principle: amateur traders often hold onto losing positions too long, hoping for a rebound, while taking profits too quickly. The Turtles did the opposite - they exited losing trades early and scaled up their winning positions as they climbed in value, not only riding the winners but amplifying the gains. Some people struggle to average up, but investing is about risk adjusted returns and sometimes an investment is more attractive at a higher price if the risk profile has reduced (more on this shortly).

5. Exits – When to Get Out of a Winning Position: The fifth rule was to have a clear strategy for when to exit a trade. Many trading systems fail because they don’t address when to take profits, leading traders to either exit too early or hold on too long. The Turtles used a trailing stop-loss system, adjusting their exit points as the price of their winning trade increased. This ensured they locked in profits without abandoning a position prematurely.

6. Tactics – How to Buy or Sell: Finally, the Turtles were taught the mechanics of executing trades. Should they place a market order or use a limit order? How should they navigate illiquid markets where their trades could move prices? These tactical decisions were crucial, particularly when dealing with large volumes or volatile markets. Even small inefficiencies in execution could eat into profits, so mastering the mechanics of trading was essential.

If you are interested in reading the full Turtle rules, I attach them for you:

The lessons from the Turtle Traders, like those from the Chevalier and Pascal, are timeless. Success in trading, or in any venture involving risk, comes down to discipline, risk management, and sticking to a system. It’s not about winning every time, but about skewing the odds in your favour and minimizing the impact of losses when they inevitably come.

From the salons of 17th century Paris to the trading floors of Chicago in the 20th century, the rules remain the same: calculate the risks, respect the odds, and trade with confidence and consistency. And above all, remember that in the long run, the most disciplined player always wins.

Too many investors view every investment as a get rich quick lottery ticket. They jump on the latest investment mania hoping to land a windfall. This explains why history is full of investment bubbles, all driven by irrational exuberance and greed.

Consider Tulip mania (1634-37), during which time the price for a single tulip bulb reached more than one month’s salary! Behavioural economics explains this kind of behaviour as “greater fool theory”: it doesn’t matter what price you pay because you’ll always make money if you are able to find a greater fool willing to pay a higher price than you did. It never ends well.

The same madness was witnessed during the South Sea Bubble (1711-1720), the Japanese property bubble (1990s), the Dotcom boom (2000s) and the ongoing Cryptocurrency mania (2020s).

There is a clear distinction that needs to be drawn. Investing is an academic game requiring a probabilistic approach, whereas speculation is a game of pure chance where the odds are invariably stacked against you.

Some speculators make money and a few see outsized returns, but they’re based on luck rather than skill, making them unsustainable and unpredictable. So it becomes evident that it is simply impossible to consistently outperform everyone, because some simply get lucky.

Most investors make the mistake of chasing short-term gains, comparing their performance against other investors or stock indices. This approach misses the key principle: the goal is to optimize risk-adjusted returns over the long term, not to beat the market.

3. A Day At The Races

Let’s think of the stock market like a horse race, where each horse represents a different investment.

Golden Bullet is the favourite, winning one out of every two races, giving it a 50% chance of success. Bronze Bronco, on the other hand, wins just one out of five races, making its odds of success only 20%. Given these statistics, which horse would you bet on?

Most people would choose Golden Bullet, not only because of its appealing name but because it has the higher chance of winning. However, this reasoning is flawed. The more people bet on Golden Bullet, the worse the odds become in a parimutuel betting system.

For a savvy investor, success isn't solely about the chance of winning. It’s about evaluating the risk-adjusted returns, which means factoring in the price or, in this case, the betting odds.

Golden Bullet's odds are similar to a coin flip - a 50/50 chance. For a fair return, you would need to at least double your money for each winning bet just to break even. But at the track, due to Golden Bullet's popularity, you find that you would have to risk $2 to be in with a chance of winning a single dollar. If you place bets like this on every race you’ll end up losing twice as much as you win. Yet most people will still place their money on Golden Bullet because they see it as the most likely winner - human nature is peculiar that way!

“The central principle of investment is to go contrary to the general opinion, as investments that are widely agreed upon tend to be overpriced.”

John Maynard Keynes

Now, let's consider Bronze Bronco. Because it's unpopular among casual gamblers, its odds are better than its actual chances of winning. At 5-to-1, you would lose four dollars for every five that you gain - the odds are in your favour, so the smart money bets on Bronze Bronco because it offers the "optimal risk-adjusted return."

This doesn’t mean betting on Bronze Bronco makes you more likely to win any particular race. In fact, you’re more likely to lose, while Golden Bullet remains the favourite.

People who back the favourite will win the most races, but they’ll end up losing money because they’re betting at unfavorable prices. The smart fella betting on Bronze Bronco may win only one out of five races, but he’ll still come out ahead financially.

In reality, the opportunity for profit comes from the mistakes of others. The lesson here isn’t about how many races you win, but about finding favourable risk-reward ratios.

In investing, it’s not about the short-term returns in the market (a single race), but where you end up in the long-term (after all the races have been run). This is what we mean by risk-based returns.

Just as we saw with the Turtle Traders, to win you need to adopt a strategy, stick to it religiously and play the long game. Our man at the race track only comes out on top if he sticks with his strategy on every race that day. We know that he will only win once every five races and so if he decides to quit after losing the first three, then he is destined to fail. This explains why most investors lose money - they either don’t have a strategy or else they don’t see it through.

The crucial point is not to leave the track halfway through the day. If you invest with a five or ten-year time horizon, don’t sell out just because you’re down in year two.

Consider each of your investments as a horse in a race. You may only need four winning stocks out of a portfolio of twenty to come out ahead. Fill your portfolio with underappreciated opportunities like Bronze Bronco, and steer clear of popular choices like Golden Bullet that everyone else is chasing.

This is also why one should never offer share tips - it’s not about a single horse in a single race - it’s all about deploying a strategy across a large number of races. Continuing our race track analogy, if someone sought a tip for a single race then their strategy would be very different to yours and the best advice one could offer is to bet on Golden Bullet because he is the favourite and the most likely to win a single race. However, despite offering this advice, you would have an entirely different strategy and so would be putting all of your money on Bronze Bronco.

Similarly, buying a stock just because Warren Buffett bought it is foolish unless you share the same strategy and portfolio as him.

Returning to the topic of averaging-up as I promised I would, imagine you placed a bet on Bronze Bronco at 5-to-1 odds, knowing his actual chances of winning were one in five. Now, picture two horses dropping out of the race. As a result, Bronze Bronco’s odds shorten to 4-to-1, and his chances of winning improve to one in three.

At first glance, these new odds seem less attractive - you now risk $1 to win $4 instead of $5. But the key detail is that the race itself has changed. With fewer competitors, the risk of losing has dropped - from 80% down to 67%.

Look at it another way: in your initial bet, you lost $4 for every $5 you made, giving you a 25% return. Now, at the higher price, you’d lose $3 for every $4 won, boosting your return to 33%. Since the risk has decreased, increasing your bet at the new odds makes sense—it offers a better risk-adjusted return.

The same principle applies to investing in stocks. A company’s risk profile can improve for various reasons—securing a patent, passing a clinical trial, or forming a strategic partnership. When that happens, the stock may actually offer better value at a higher price because the investment is now less risky.

To summarize, successful investing relies on three elements: information, skill, and luck. At the race track the information is your assessment of each horse's chances of winning based on statistical analysis combined with the known odds available on each horse. Skill involves using that information to build a winning strategy. Luck is the wild-card that can change everything. Maybe a rival horse gets injured and pulls out, boosting Bronze Bronco's chances. Or, worse yet, Bronze Bronco could be the one limping off the track. Luck is beyond our control, but a good strategy can account for it. The trick is to set yourself up to win big when luck is on your side, while still being able to weather the losses when it isn't.

Remember, there are old investors, and there are bold investors, but no investor grows old being bold. Chasing big wins while ignoring risks may bring short-term success, but it eventually leads to ruin. The smart investor knows how to stay in the game!

Great article, it was definitely worth the wait after your teaser last week :)

Thank you for the great article.